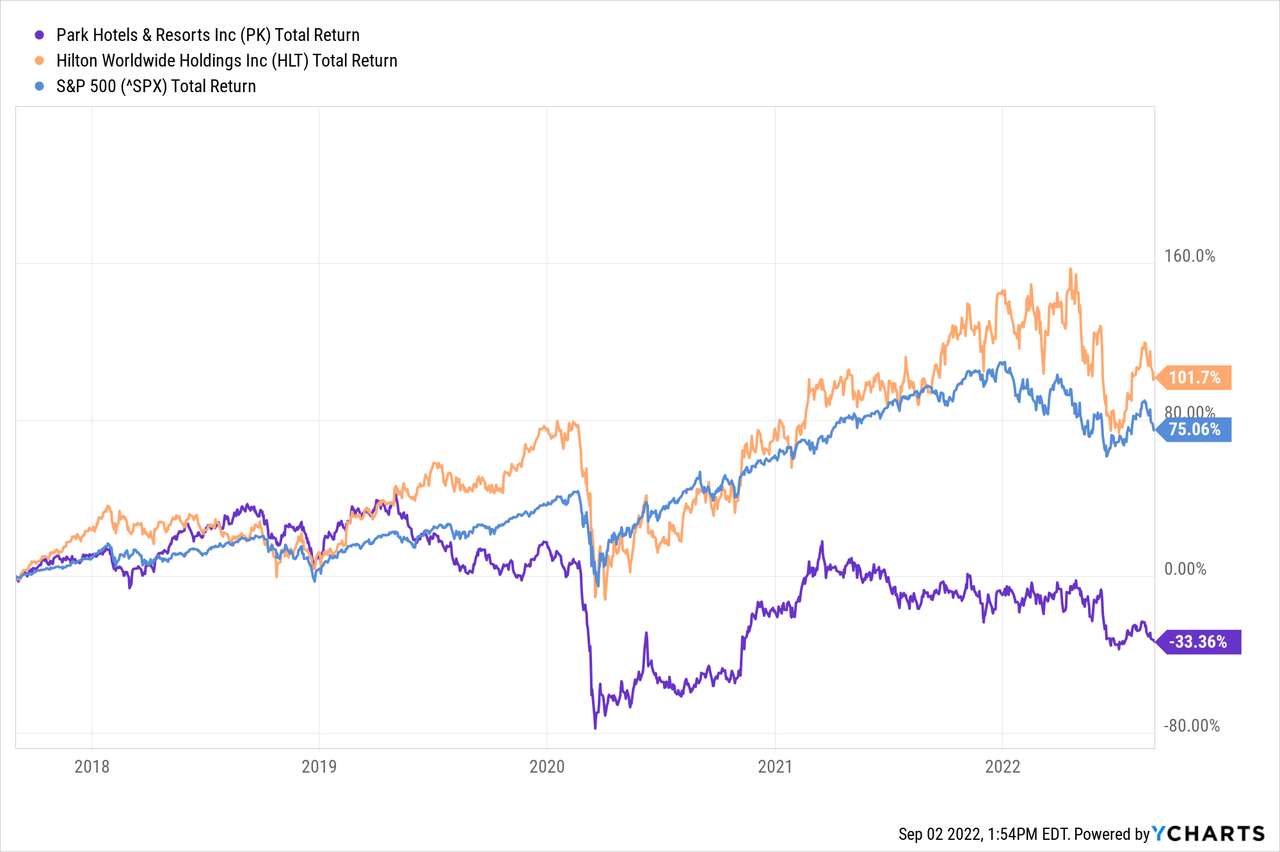

I am looking back at a real estate investment trust (“REIT”) I bought in my portfolio in mid-2020. This REIT is Park Hotels & Resorts Inc. (NYSE:PK). Park Hotels spun off from Hilton in 2017 in an effort to lower their taxes and increase shareholder value. Shareholders holding Hilton Worldwide (HLT) shares did well, but Park Hotels’ share price lagged.

Park Hotels is a REIT with a real estate portfolio of approximately 60 hotels and resorts. Hotels and resorts have been hit hard by the mandatory closures during the corona crisis. At the time, it was my “speculation” hoping things would work out, so I took a small position in Park Hotels. At the beginning of 2021, I sold my position for a profit.

I like to go on holiday, the hotels and resorts of Park Hotels look neat, but I still give it a sell rating because of the large amount of debt on their balance sheet. I expect this will deter them from making future investments. The proceeds from the equity offering will have to be used in conjunction with refinancing their debt to reduce their debt burden. This is not a good prospect.

Park Hotels’ financial position has greatly improved since the corona crisis. In 2020, their sales fell by 71%, but in 2021 their sales are about half of their 2019 sales. There is clearly visible recovery.

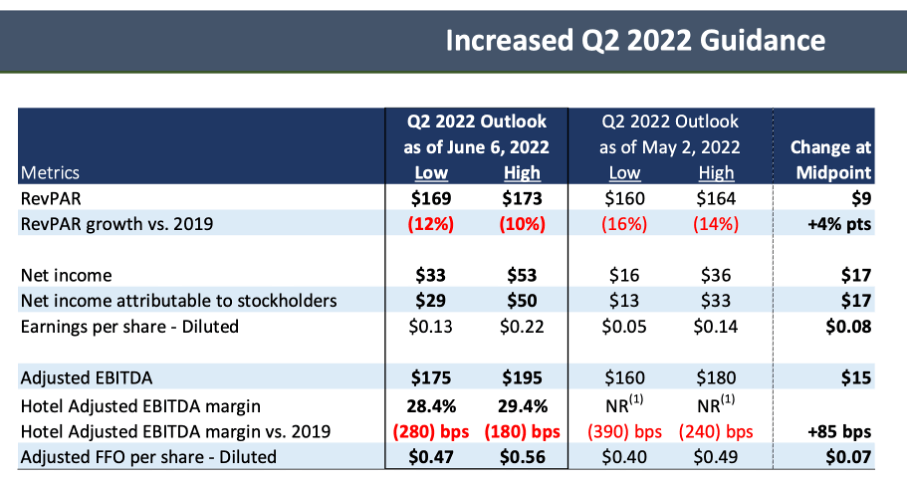

Park Hotels recently raised their outlook in May. Their EBITDA has improved significantly since the coronavirus crisis and their RevPAR and Adjusted EBITDA expectations have been revised upwards.

Increased Q2 2022 Guidance (May 2022 Investor Presentation )

Increased Q2 2022 Guidance (May 2022 Investor Presentation )

I’m not going to use their current numbers in this analysis, as I expect the recovery to continue and their revenues to return to 2019 levels.

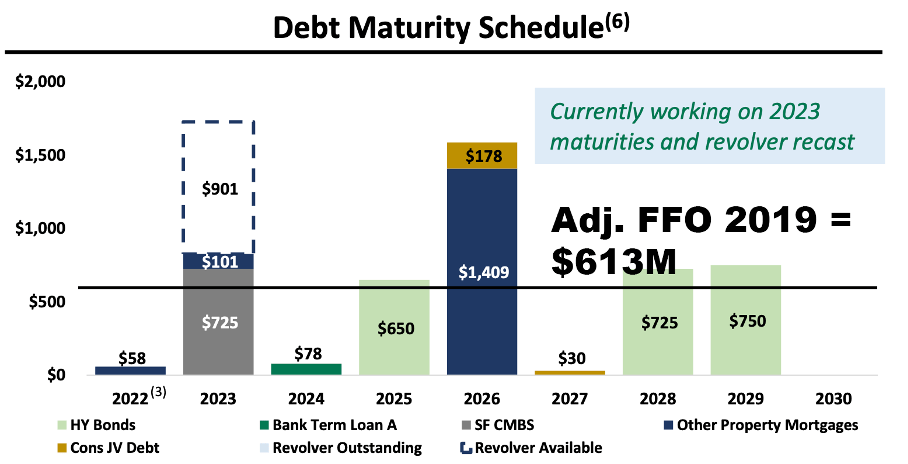

What worries me is their long-term debts. Major repayments will be made in 2023 and 2026. The other debts are well distributed over the other years. In the years 2024, 2027, 2030 and beyond, there is an opportunity to refinance their large debt from 2023 and 2026 – at higher interest rates.

Debt Maturity Schedule (May 2022 Investor Presentation)

Debt Maturity Schedule (May 2022 Investor Presentation)

Refinancing would be an ideal option, but I suspect Park Hotels will need to issue additional shares to meet their debt obligations. In their 2019 annual report (their best year), Park Hotels generated an adjusted funds from operations (“FFO”) of $613 million.

Adjusted FFO 2019 and 2018 (2019 Annual Report)

Adjusted FFO 2019 and 2018 (2019 Annual Report)

If we compare the adjusted FFO of $613 million for 2019 with their debt level for the coming years, we see that their debt level is higher than their 2019 adjusted FFO. They will have to refinance the high debt in 2023 and 2026 at a higher interest rate. The adjusted FFO of 2019 is the most favorable level, Park Hotels is still on track to recover.

Debt maturity schedule and adjusted FFO 2019 (May 2022 Investor Presentation and Authors’ Own Modification)

Debt maturity schedule and adjusted FFO 2019 (May 2022 Investor Presentation and Authors’ Own Modification)

In parallel with the refinancing, they can raise money by issuing additional shares. However, this is disadvantageous for shareholders if the proceeds are only used to pay off debts, because this does not generate any income and dilute shares. A REIT generally issues stocks to invest in real estate, which in turn generates rental income. 90% of the profit is paid out as a dividend.

Park Hotels’ debts are generally high and I expect that they will not be able to make new investments and will have to focus entirely on paying off their debts.

Finally, possible closures due to corona pose a risk to the leisure sector. And hotels and resorts are classified as high-risk stocks because they often fall sharply during economic recessions. But this also offers opportunities, by buying the deeply depressed hotel stocks whose companies are financially healthy, very high stock returns can be expected. For now, it remains to be seen what will happen in the near future. U.S. GDP fell in the second quarter, but unemployment remains low. I give Park Hotels a sell rating due to their high debt, volatile nature of hotels and resorts, and questionable economic outlook.

Park Hotels is a REIT that manages and rents approximately 60 hotels and resorts and was spun off from Hilton in 2017. Hotels and resorts were hit hard by the mandatory closures due to the corona crisis, including Park Hotels. Park Hotels have shown a strong recovery and is well on their way to recover from the corona pandemic. Still, I think their long-term debt is too high compared to the adjusted FFO from 2019 (their best year). Huge debts are outstanding for 2023 and 2026, which they will have to refinance at a higher interest rate. The higher interest rates will affect their operating income. The debt over the other years is also high compared to their adjusted FFO of 2019. As a result, I don’t expect them to be able to make new investments.

A REIT has the option to issue additional shares. It makes sense that Park Hotels do this to reduce their debt, but it is not beneficial for shareholders. Because Park Hotels is highly indebted and therefore has little room for expansion, the volatile nature of hotels and resorts and the subdued economic outlook make this stock a sell.

Thomas Barwick

Thomas Barwick

This article was written by

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.