We use cookies and other tracking technologies to provide services in line with the preferences you reveal while browsing the Website to show personalize content and targeted ads, analyze site traffic, and understand where our audience is coming from in order to improve your browsing experience on our Website. By continuing to browse this Website, you consent to the use of these cookies. If you wish to object such processing, please read the instructions described in our Cookie Policy / Privacy Policy.

Interested in blogging for timesofindia.com? We will be happy to have you on board as a blogger, if you have the knack for writing. Just drop in a mail at to******@***********et.in with a brief bio and we will get in touch with you.

General Partner, Cactus Venture Partners

A start-up raising capital is inspiring for both the start-up ecosystem and for start-up-focused news platforms; increasingly so in a not-so-buoyant environment. It is a source of optimism for founders who have put their ‘blood, sweat, and tears’ into their vision. Capital is possibly one of the most critical (and sometimes prohibitive) factors for emerging entrepreneurs. A decent proportion of the entrepreneurs’ time goes into estimating fund requirements, planning for them, and finally into the actual process of raising funds. Even a great idea, in the absence of capital, might not be able to live up to its potential.

In order to establish large businesses and achieve scale, businesses inevitably need to make the initial investments to ensure that they build the yet-to-be-explored markets to gain access to their target customers. Hence, we constantly hear about burn rates, operating losses, and large capital raises in the private markets. Even large global companies such as Amazon, Facebook, Alibaba, and Tencent made these initial investments before they started funding their own growth. That said, all burns are not equal. In our view, a check on the quality of capital burn is necessary for businesses, especially when access to capital is not very difficult (as has been the case in the recent past). Sometimes, large amounts of capital cause entrepreneurs and investors to lose track of the quality of burn. Capital burn, which helps drive STICKY AND ACCELERATED revenue growth, is justifiable. However, if it provides only a short-term boost to the Gross Merchandise Value (GMV)/Gross Transaction Value (GTV), and the revenue (or a large part of it) stagnates or decreases in the absence of the burn, then the merit of such a burn needs to be critically evaluated.

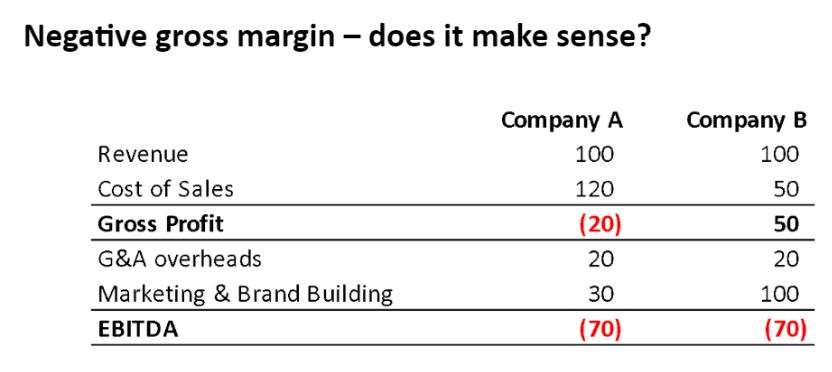

In the simplistic scenario above (of two imaginary companies), assuming CAC (customer acquisition cost) and retention percentages are similar, which company would you invest in? Despite revenues of 100 units and a loss of 70 units for each of the two companies, you would agree that the quality of the burn is very different. Company A is losing money at the gross margin level, while Company B is losing money because it is investing in growth-focused marketing and brand building initiatives. Though the top and bottom lines appear similar, the growth trajectory of these companies can be materially different, because Company A is burning to sustain operations, while Company B is burning for profitable future growth.

Does it make sense to incur losses at the gross margin level? Selling a product or service below its cost-to-the-company implies that the more the company sells, the more it loses, even before accounting for the overheads; i.e., scale is not essentially a friend in the absence of a plan for a strategic shift on economics in the future. It’s as simple as that and one would think that this concept is too obvious to even consider. However, we do see instances where companies, even market leaders for a number of years, are making significant losses at the gross margin level in anticipation of future growth. Is it prudent to undertake such practices? In a way, such strategies imply an obsession with increasing the GMV or gross sales without paying much attention to the underlying economics. Why would I, as a consumer, have a problem if the business wants to fund my consumption (from VC capital)? Should such businesses or entrepreneurs be rewarded for incurring ever-increasing losses? In our view, the answer is “No”, with very few exceptions (as always). What are these exceptions?

One of these exceptions can be using this strategy for products/services where there is a significant network effect, which could translate into materially better economics as and when the scale crosses a certain critical size. Social Platforms are probably a good example of this. Such companies make losses in the early days but build a strong network of a very large number of people, which the companies can successfully monetize later in multiple ways. That said, it is important to keep in mind the quality of the user-base in such cases. Bottom-of-the-pyramid users without the ability to spend and with low CPM rates are unlikely to justify the loss incurred to acquire them.

Another exception to using a strategy incurring gross margin losses can be to drive discovery, i.e., when the consumers themselves do not know the value of the product/service and the entrepreneur needs to help the consumer discover the utility or value of the product. In such cases, it makes sense for the company to help the consumer explore the product/service and discover the value and in the process, the price point for the product/service. However, there should not be multiple iterations of the same gross-margin discounting for the same customer. In our view, Netflix is a good example of this. The first month subscription is free, i.e., the company allows the consumer to explore the utility of the service and determine its value (and marginal utility, which can be different for different people).

E-Commerce in the early days did the same for new users and allowed them to discover the convenience/value of the experience of purchasing from a much larger set of options/SKUs without stepping out of their homes (and into traffic, in case of India). However, if the negative gross margins continue for a prolonged time, they might actually become counter-productive; even customers who could drive profit might tend to wait for the discount period and delay their purchase to benefit from the negative gross margins or switch between platforms for discount-hunting. Moreover, the negative gross margins could also inhibit the founders/investors’ ability to understand the true market demand and potentially limit their capacity to take prudent financial decisions with fair information.

{{C_D}}

{{{short}}} {{#more}} {{{long}}}… Read More {{/more}}

Views expressed above are the author’s own.

Engg not just about computer science and IT. Can we stop this mad rush?

After all, the Raj is dead: Colonialism was horrific. But a confident India should move past the decolonisation debate

The peace principle: Modi’s words to Putin didn’t mean a change in stance. India’s ability to wage peace is set to increase

At G20, India can show the way: PM Modi’s welfare, empowerment schemes should be a blueprint for many countries

How AI benefits ed-tech businesses’ customer service

Pension tension: Punjab may join Rajasthan, Chhattisgarh in junking NPS. This is fiscally ruinous & politically ineffective

Can wordsmith Tharoor teach the grand old party some new tricks?

Let’s put things in perspective with a towering Gandhi statue

India’s Russia problem will grow: Locked out of semiconductor supply, Moscow will be hard-pressed to fulfil New Delhi’s military needs

What Modi does but Gandhis can’t: New BJP reaches out to people with professionalism. Congress still takes a casual approach

Interested in blogging for timesofindia.com? We will be happy to have you on board as a blogger, if you have the knack for writing. Just drop in a mail at to******@***********et.in with a brief bio and we will get in touch with you.

TOI Edit Page

Heartchakra

Ruminations,TOI News,Tracking Indian Communities

Chennai Talkies

Copyright © 2022 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service

Powerful Wealth Building Resources