JasonDoiy

JasonDoiy

This is an abridged version of the full report published on Hoya Capital Income Builder Marketplace on September 7th.

Hoya Capital

Hoya Capital

Single-Family Rental REITs (“SFR REITs”) – which have been one of the best performing property sectors since their emergence in the mid-2010s in the wake of the last housing crisis – should prove to be a source of relative shelter in the current economic environment of modest growth, rising mortgage rates, and tight credit conditions in the single-family housing market – the exact type of environment that fueled the initial wave of “institutionalization” of the single-family rental sector. In the Hoya Capital Single-Family Rental Index, we track the three SFR REITs: Invitation Homes (INVH), American Homes 4 Rent (AMH), and newly-US-listed Tricon Residential (TCN). We’ve also added NexPoint Diversified (NXDT) to the index following its conversion to a REIT from a closed-end fund, of which SFRs are the new REITs’ largest holdings through its minority interests in Vinebrook and NexPoint Home Trust.

Hoya Capital

Hoya Capital

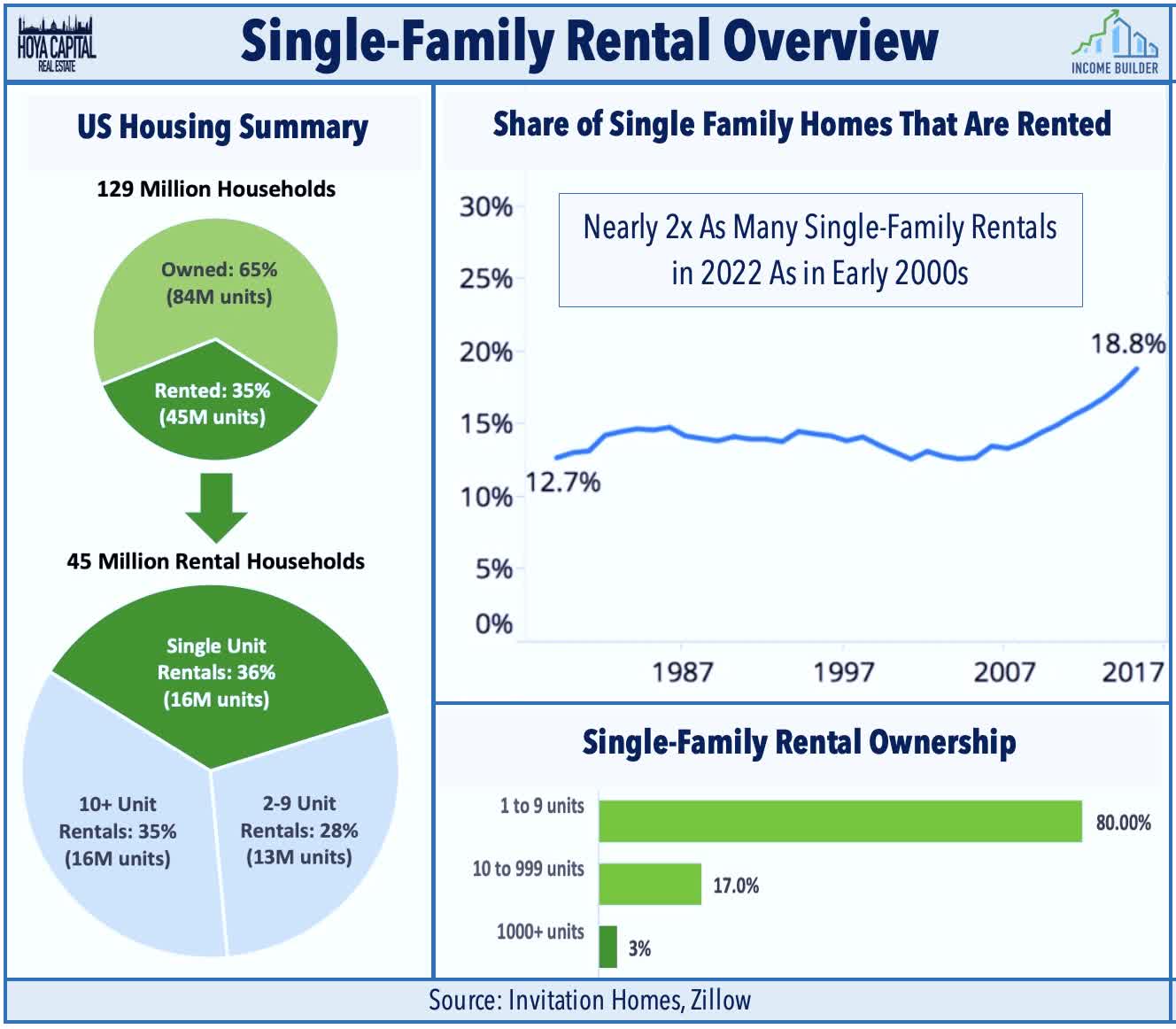

One of the most notable success stories of the Modern REIT Era, SFR REITs were born from the last economic crisis when a cascade of foreclosures enabled a new class of institutional rental operators to emerge by buying distressed properties en masse. While we continue to expect home price appreciation to cool considerably over the next several quarters – and note that month-over-month growth rates have already turn negative in some markets – widespread distress in the U.S. housing market is highly unlikely given the underlying supply constraints resulting from a decade of underbuilding, and ironically, due to the more substantial presence of well-capitalized institutional investors. The share of single-family homes that are rented has nearly doubled since the early 2000s and now comprises nearly a quarter of the single-family market, but the vast majority of the SFR market is still managed by “mom and pop” investors that own between 1-9 units.

Hoya Capital

Hoya Capital

We continue to believe that the “institutionalization” of the SFR market remains in the early innings and the recent rise in mortgage rates will be a catalyst to drive further market share gains to larger institutions that have access to cheaper and deeper sources of capital. While these trends attract a fair share of negative headlines, renters report to be quite a bit happier with these larger landlords compared to smaller property managers, underscored by another quarter of record-low turnover rates and near-record-high occupancy rates achieved by these SFR REITs. As we’ll discuss in more detail below, a major factor fueling the rise of large institutional operators is the significant efficiencies gained in recent years through emerging property technology offerings (“PropTech”) that have enabled SFR REITs to operate with Net Operating Income (“NOI”) margins that are on-par with apartment REITs.

Hoya Capital

Hoya Capital

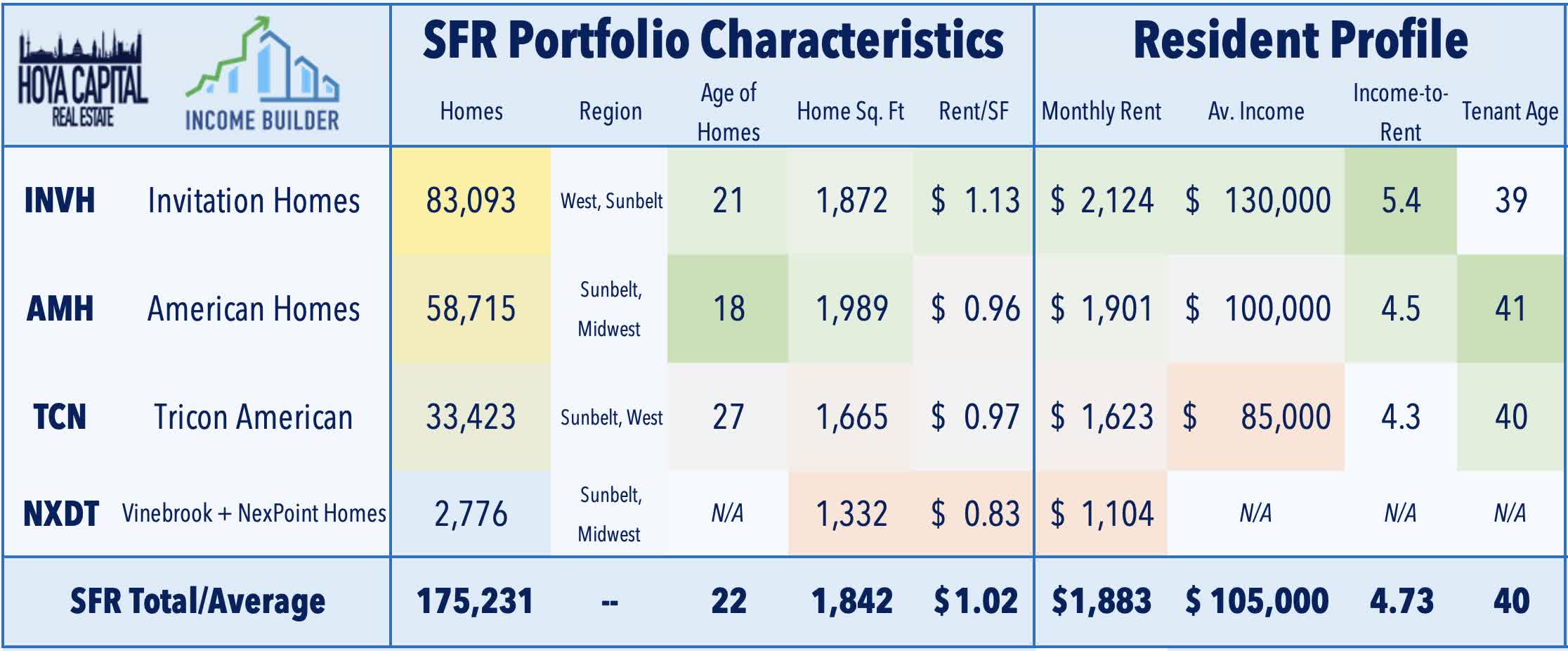

The average single-family monthly rent is $1,100 per month, but REIT portfolios skew towards the higher end of the quality spectrum with an average rent of around $1,800 per month in homes that are typically around 2,000 square feet. These three SFR REITs own a combined 175,000 SFR units in relatively high-value suburban markets and, importantly, their tenant credit profile is far better than the national averages for renter households with average annual income ranging from 85k-130k – well above the average renter household at 36k – and an average income-to-rent ratio of around 5x. The average SFR head-of-household is 38-42 years old, an age cohort that will see the strongest growth of any 5-year segment over the next decade.

Hoya Capital

Hoya Capital

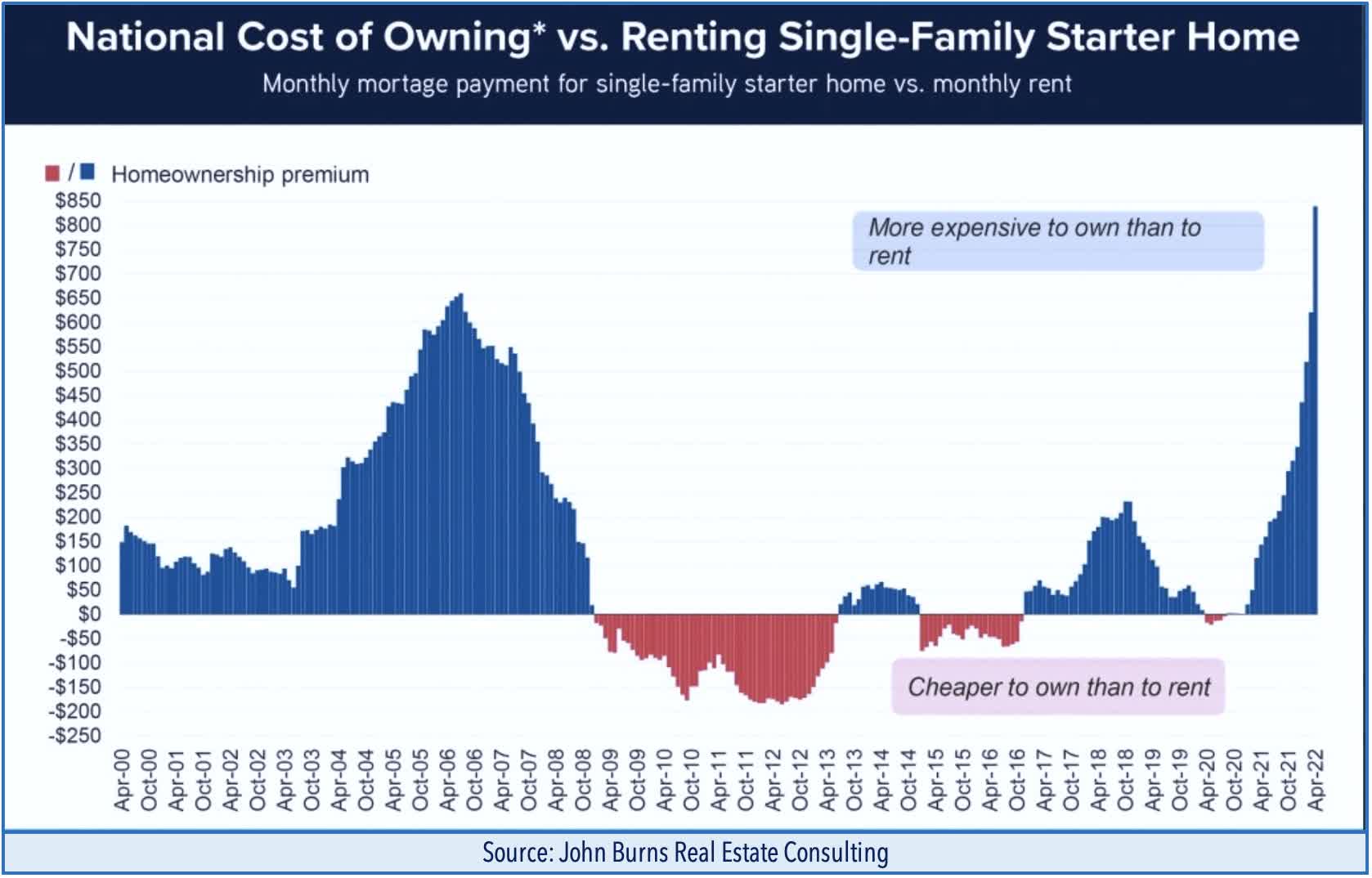

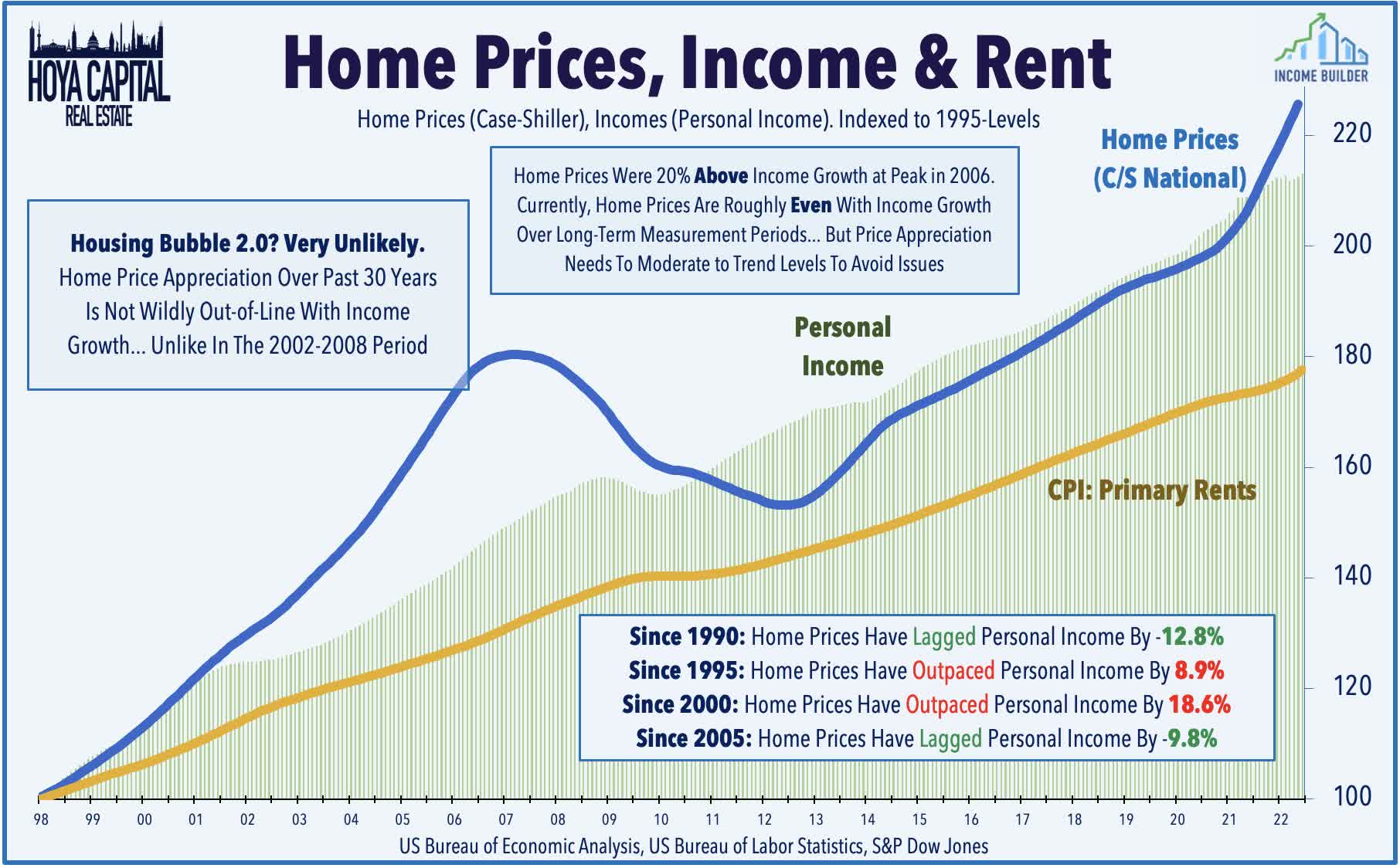

Persistent inflation is eroding built-up stimulus savings, but given that housing and food are the ultimate “essential” expenses, the slowdown will have to get awfully ugly to see widespread tenant credit issues. As we’ll discuss in more detail below, SFR REITs enter this uncertain economic period on solid footing, benefiting from historically favorable Buy vs. Rent economics resulting from the historic surge in mortgage rates through the first half of 2022. Recent data from John Burns Real Estate Consulting highlights that while the monthly cost of owning and renting was nearly identical a year ago, owning a home now costs $839 more per month than renting. This differential is almost $200 higher than at any time since the turn of the century, and households now hold a historically high preference for renting over buying.

Hoya Capital

Hoya Capital

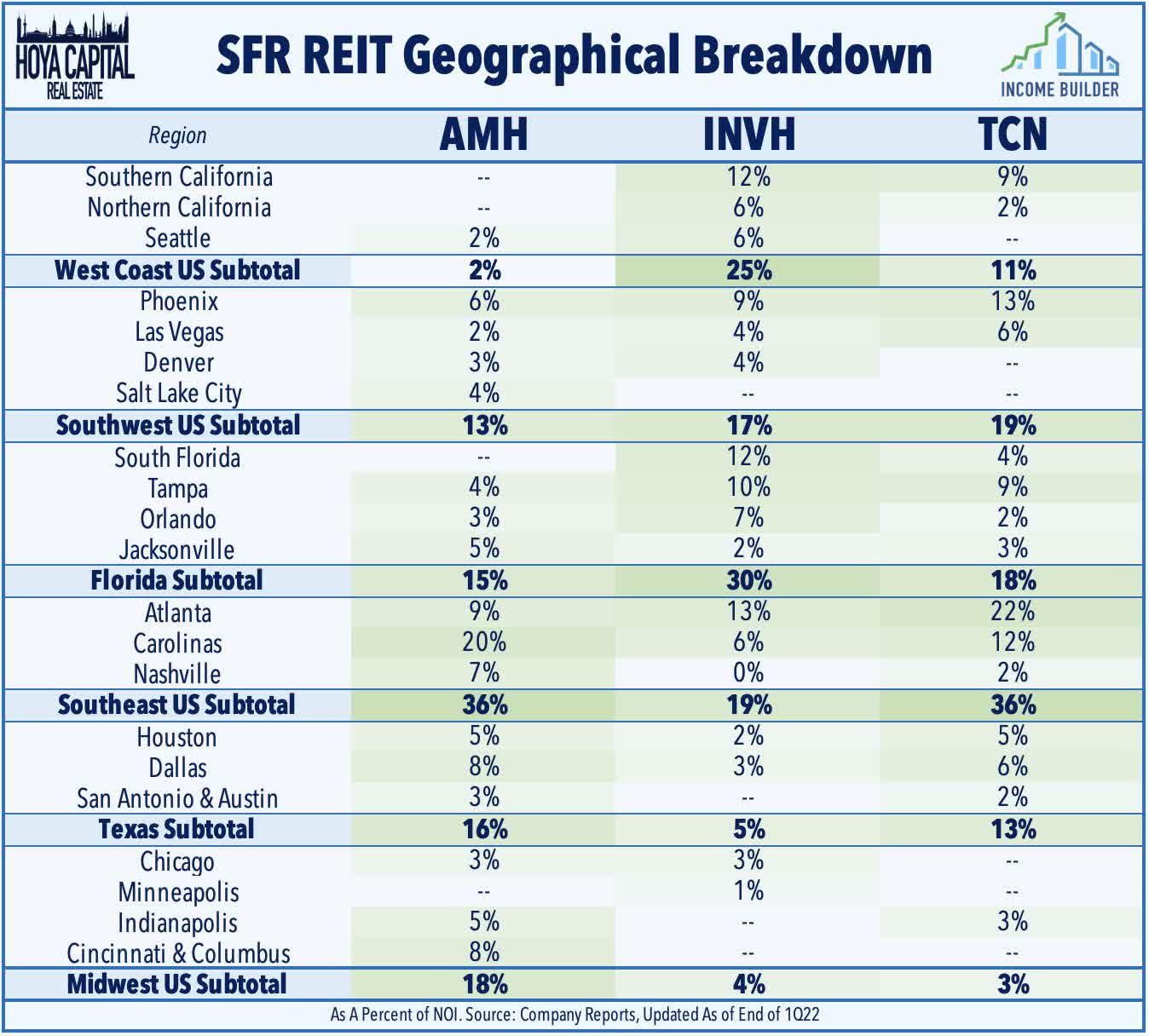

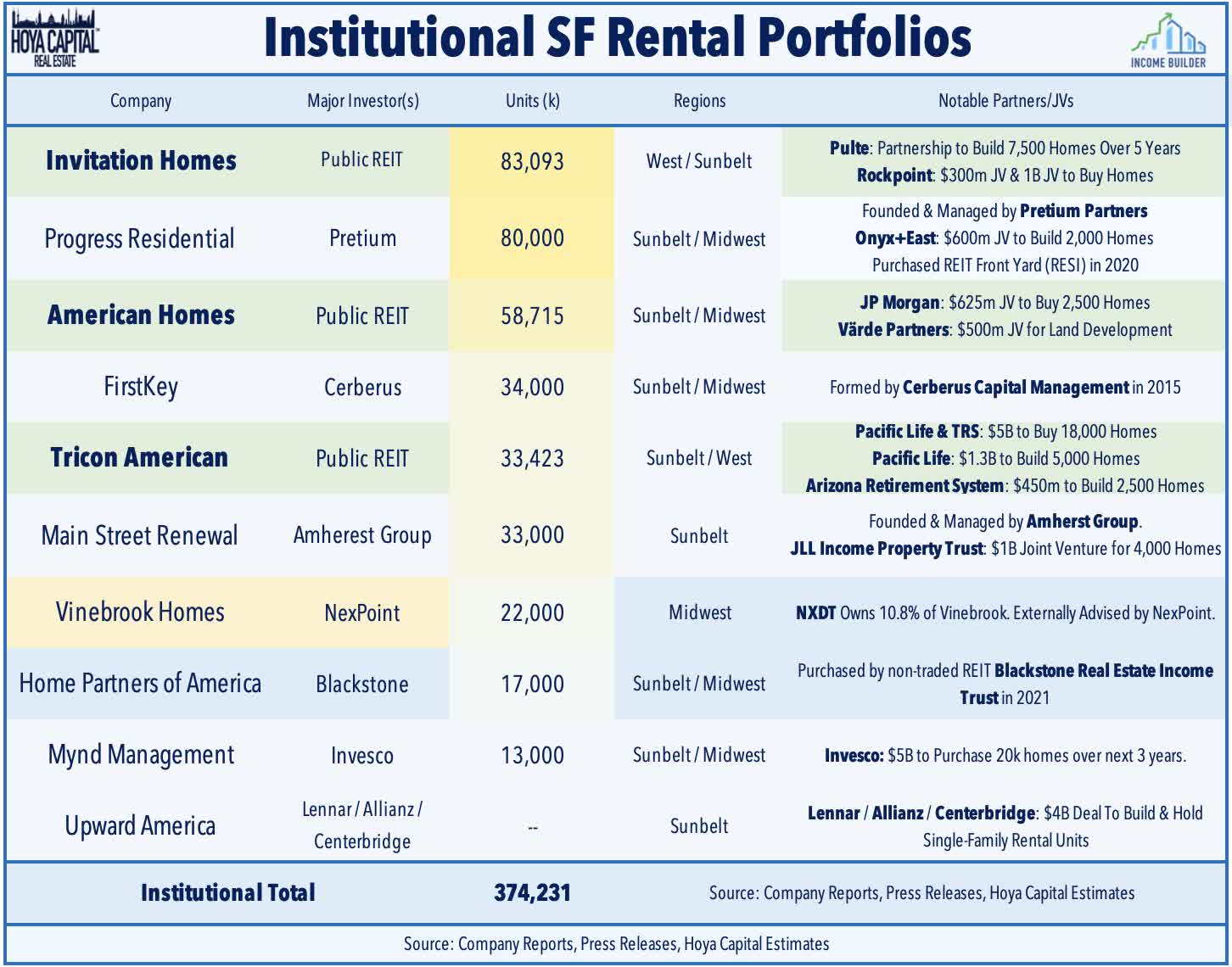

Single-Family Rental REITs concentrate heavily on the Sunbelt markets that have experienced the strongest economic growth during the post-GFC recovery and in the early post-pandemic recovery. Invitation Homes is the single-largest owner of SFRs in the country with roughly 83k units with a significant presence on the West Coast and in Florida. American Homes owns nearly 60k units and focuses primarily on the Sunbelt and Midwest regions. Last October, Tricon Residential completed its dual-listing in the U.S. in a $570M IPO after trading exclusively on the Toronto Stock Exchange since 2010. Tricon owns and/or operates more than 33k homes concentrated primarily in the U.S. Sunbelt markets. Newly-listed NexPoint Diversified owns 10.8% of Vinebrook – which owns 22,000 homes across the Midwest and Sunbelt – and 28.3% of NexPoint Homes Trust – which owns roughly 2,000 homes in Midwest and Sunbelt markets as well. For NXDT, while just 35% of its holdings are SFR assets, including its holdings in apartments and storage, residential sectors comprise more than two-thirds of its portfolio.

Hoya Capital

Hoya Capital

Other major institutional investors involved in the SFR sector include private equity firms Pretium Partners which owns/operates more than 80,000 homes through its Progress Residential platform, Cerberus Capital, which owns more than 34,000 homes through FirstKey Homes, Amherst Group, which owns/operates more than 34,000 homes through Main Street Renewal, and the aforementioned NexPoint Advisors, which manages nearly 25,000 homes through Vinebrook Homes and NexPoint Homes Trust. NexPoint also manages apartment REIT NexPoint Residential (NXRT) and mortgage REIT NexPoint Real Estate Finance (NREF). Several traditional Wall Street “heavyweights” are active in the space as well including Blackstone (BX), which owns 17,000 homes through Home Partners of America, which recently made headlines for slowing its home purchases in several markets.

Hoya Capital

Hoya Capital

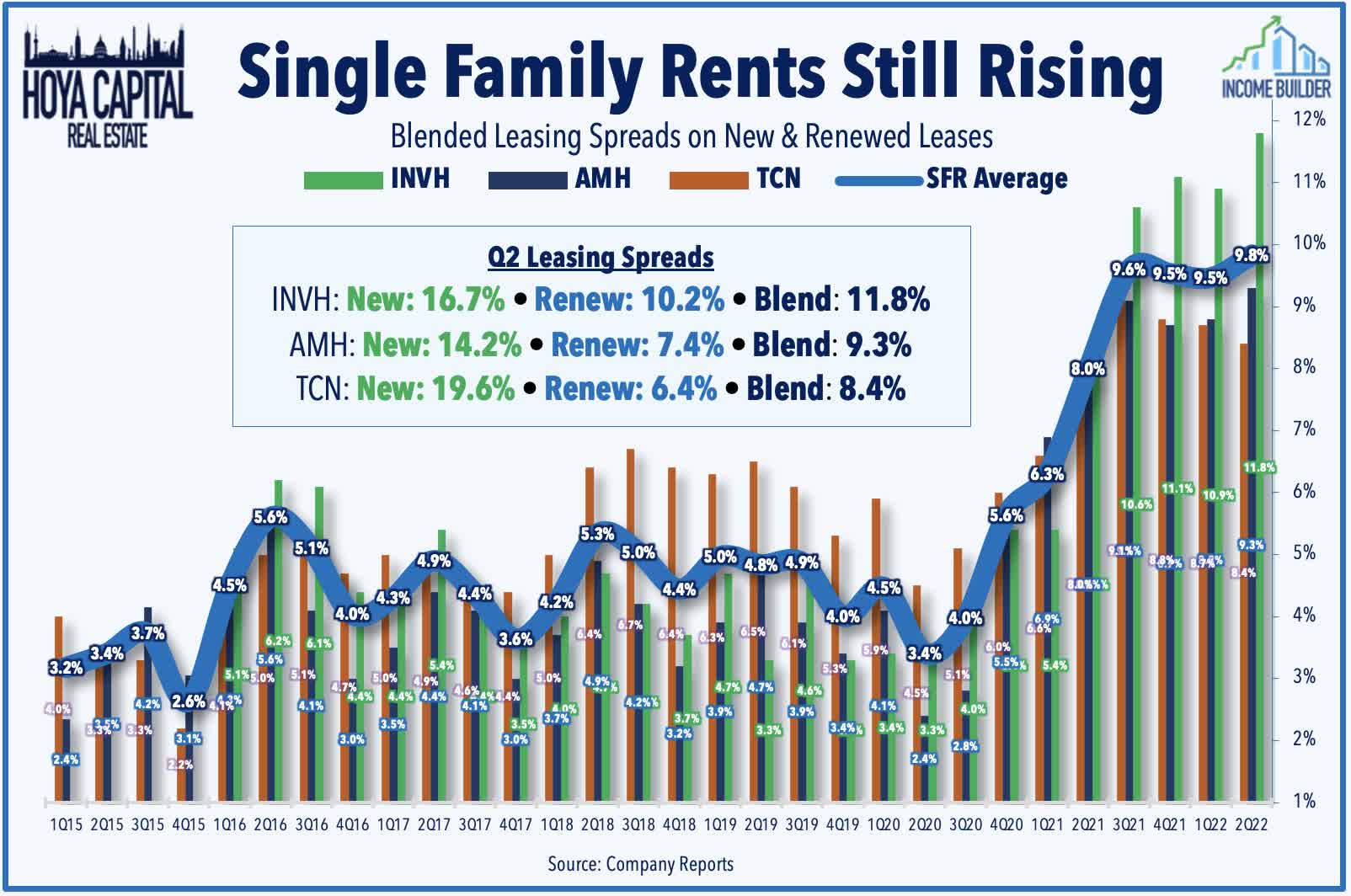

SFR fundamentals are as strong as they’ve been since the sector emerged in the early 2010s from the ruins of the Great Financial Crisis. The combination of historically low housing supply and strong demographic-driven demand – with added pandemic-related tailwinds – has sent single-family rents soaring at the fastest rate on record. Finally “catching up” to the surge in suburban home values over the past several years, SFR REITs have reported double-digit rent growth in recent months while occupancy rates continue to set record-highs. As discussed in our REIT Earnings Recap, SFR REIT rent growth on new leases averaged 16.8% in Q2 – an acceleration from the 15.0% rate in Q2 – while renewal rates rose 8.0% in Q2 – up from 7.8% in Q1, resulting in fresh record-highs for blended rent growth of just shy of 10%.

Hoya Capital

Hoya Capital

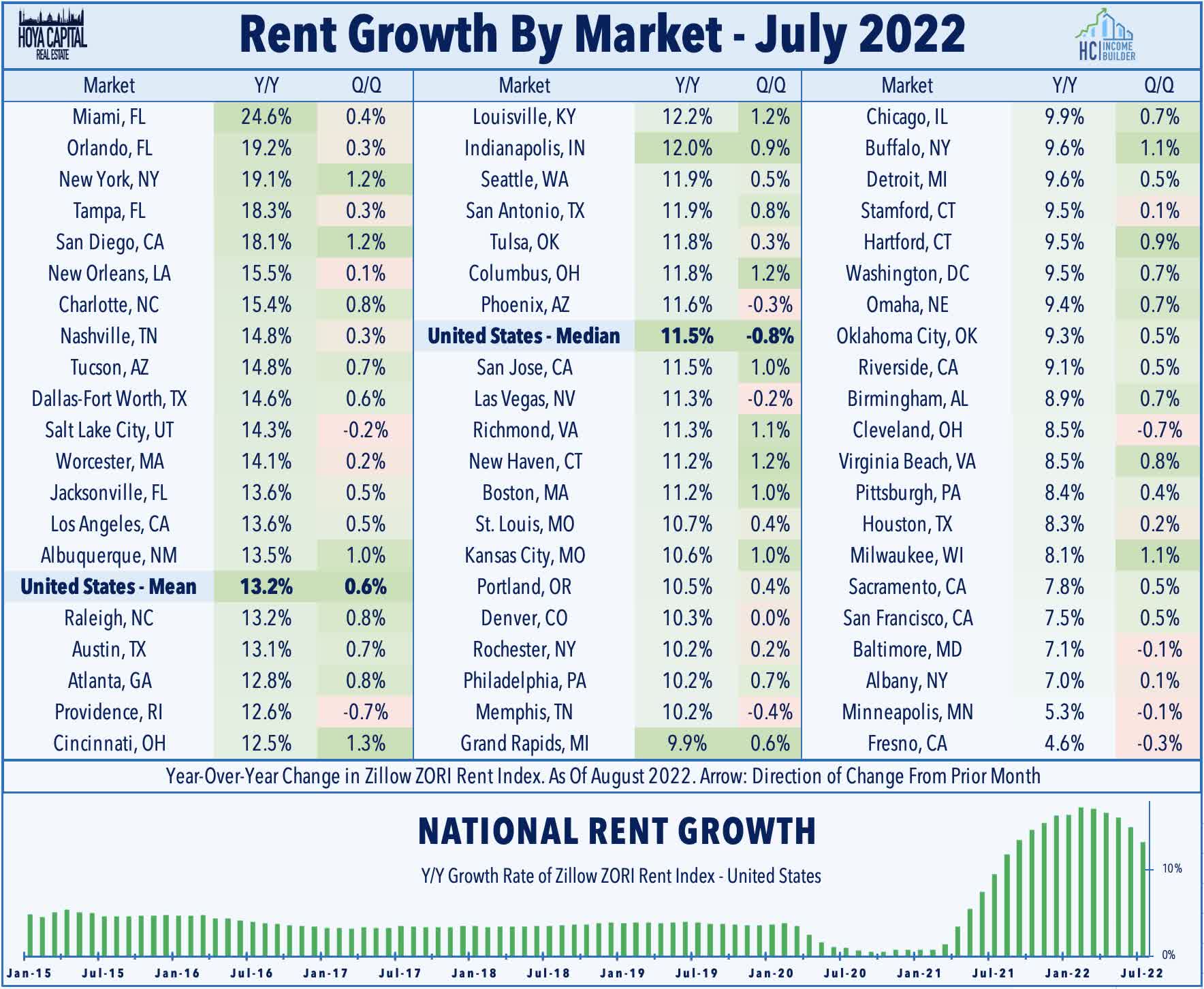

These reports were consistent with private market data showing similar strength across residential rental markets – but with more momentum behind the SFR sector compared to the multifamily sector which is more closely “indexed” the overall cost of single-family ownership, which has soared this year from the historic rise in mortgage rates. CoreLogic reported last week that while the growth rate has naturally cooled a bit in recent months, SFR rents were higher by 13.4% from one year earlier in July. CoreLogic also noted that over the past two years, rent growth has been significantly stronger on detached rental homes (24.9%) compared to attached homes (18.8%). Recent data from Zillow (Z) – which includes both SFRs and apartments – showed similar trends with rents 13.2% higher year-over-year in July but have begun to moderate from the record-high levels above 15% seen earlier in 2022.

Hoya Capital

Hoya Capital

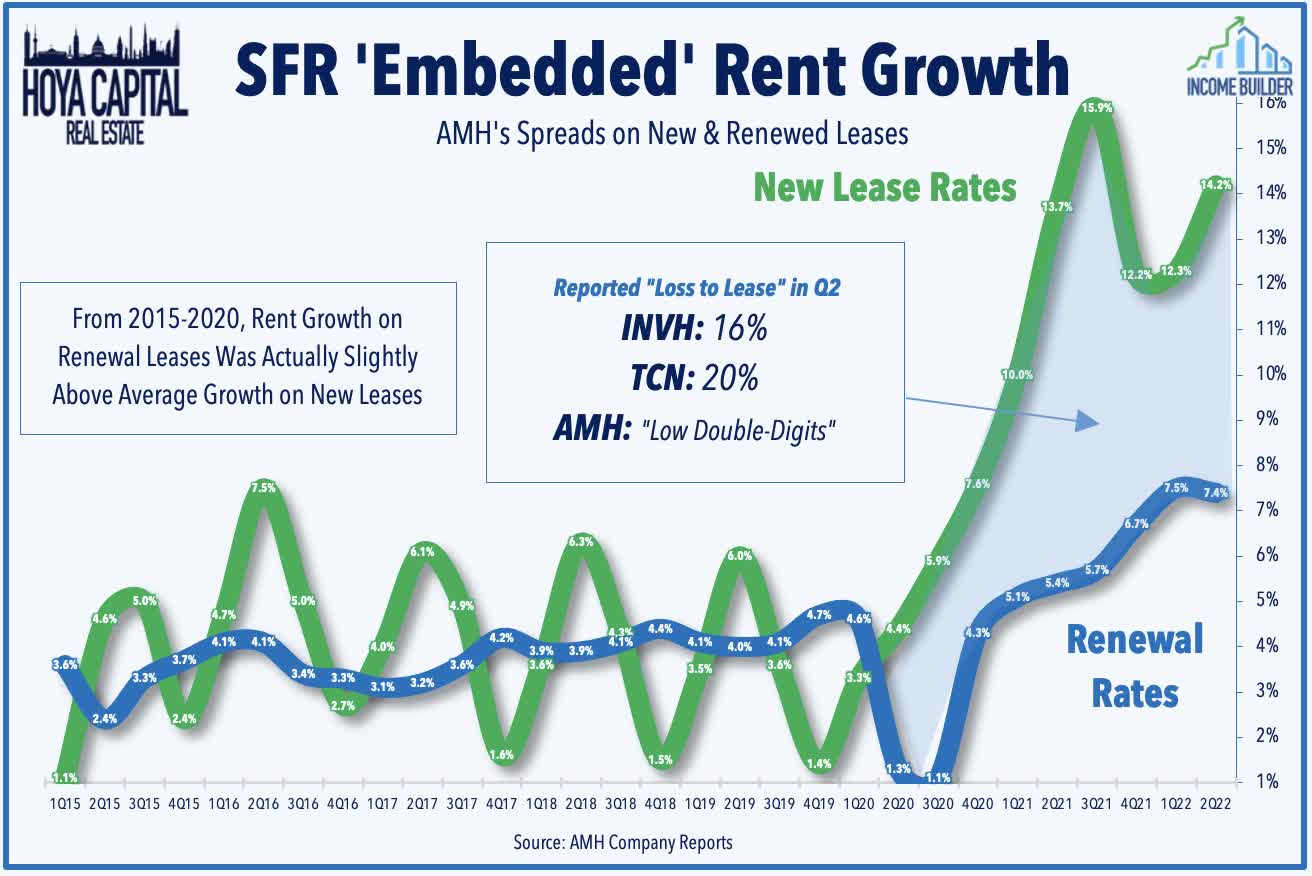

While rent growth metrics tend to put more weight on new lease rates, the “embedded” rent growth potential is substantial given the recent widespread between rent growth on new and renewal leases – a relatively new phenomenon as SFR REITs have generally achieved slightly higher average spreads on renewals compared to new lease rates from 2015-2020. SFR REITs have perhaps been a bit too generous in their renewal offers to existing residents, but we believe this has built-up a longer runway for sustained rent growth that will be unlocked over the coming quarters. INVH estimated that its current leases are 16% below market rate while AMH commented that its comparable “loss to lease” spread is in the “low double digits.” TCN estimated its embedded spread is “in that 20% range,” noting that it has been “holding back on the blended rent growth, because we self-govern on renewals.”

Hoya Capital

Hoya Capital

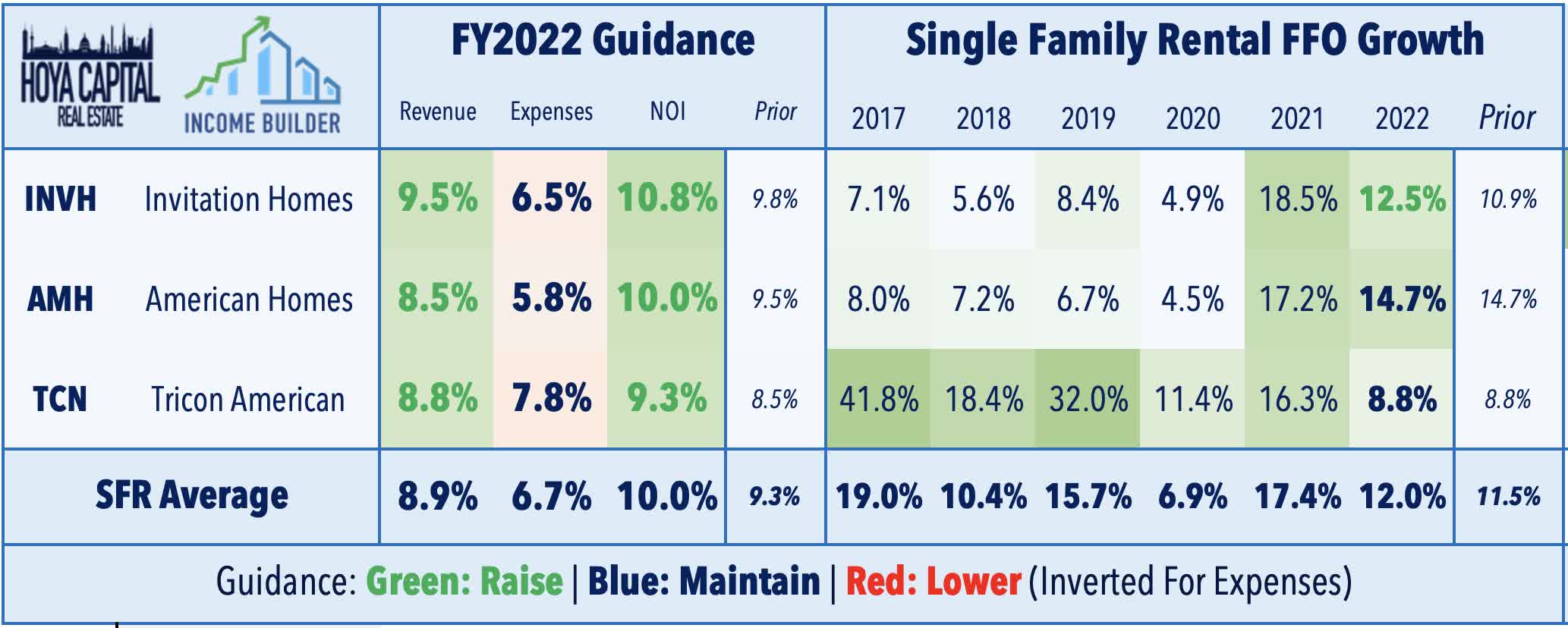

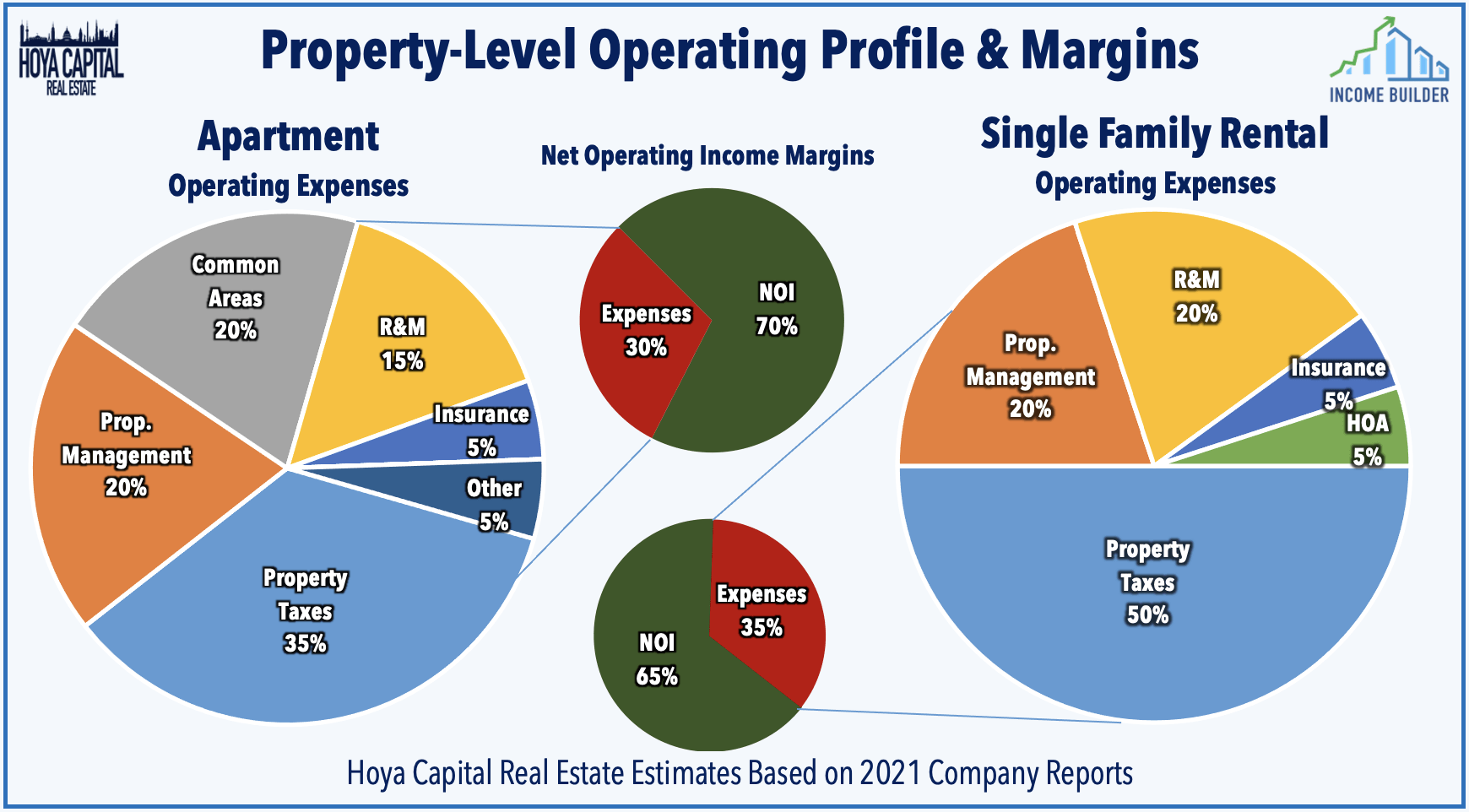

Fueled by this rent growth momentum and visibility, all three SFR REITs raised their full-year NOI growth targets in the second quarter by an average of 75 basis points to 10.0%. Led by Invitation Homes, the three SFR REITs now expect average FFO growth of 12.0% this year – up 50 bps from the prior outlook. Occupancy rates remained near record-highs at 98% in Q2 – roughly flat from the same quarter last year – and consistent with CoreLogic report showing that the number of single-family rental properties listed in early 2022 was well below pre-pandemic levels and still shrinking from one year ago. . Aided by turnover rates which continued to set record-lows, NOI margins set record-highs for full-year 2021 at 66% and improved to 67% in Q2, levels that are essentially on par with many of their multifamily peers.

Hoya Capital

Hoya Capital

While Wall Street’s growing presence in the SFR space has garnered plenty of political and media attention (and “blame” for the rise in home values and rents over the last several years), large institutional investors represent a tiny fraction – roughly 1-2% – of the overall single-family market. Smaller “mom and pop” investors – those that own between 2-10 homes and finance purchases with traditional mortgages – are responsible for the bulk of investor home buying activity. That said, we believe that the “institutionalization” of the SFR market remains in the early innings and the recent rise in mortgage rates will be a catalyst to drive further market share gains to larger institutions that have access to cheaper and deeper sources of capital.

Hoya Capital

Hoya Capital

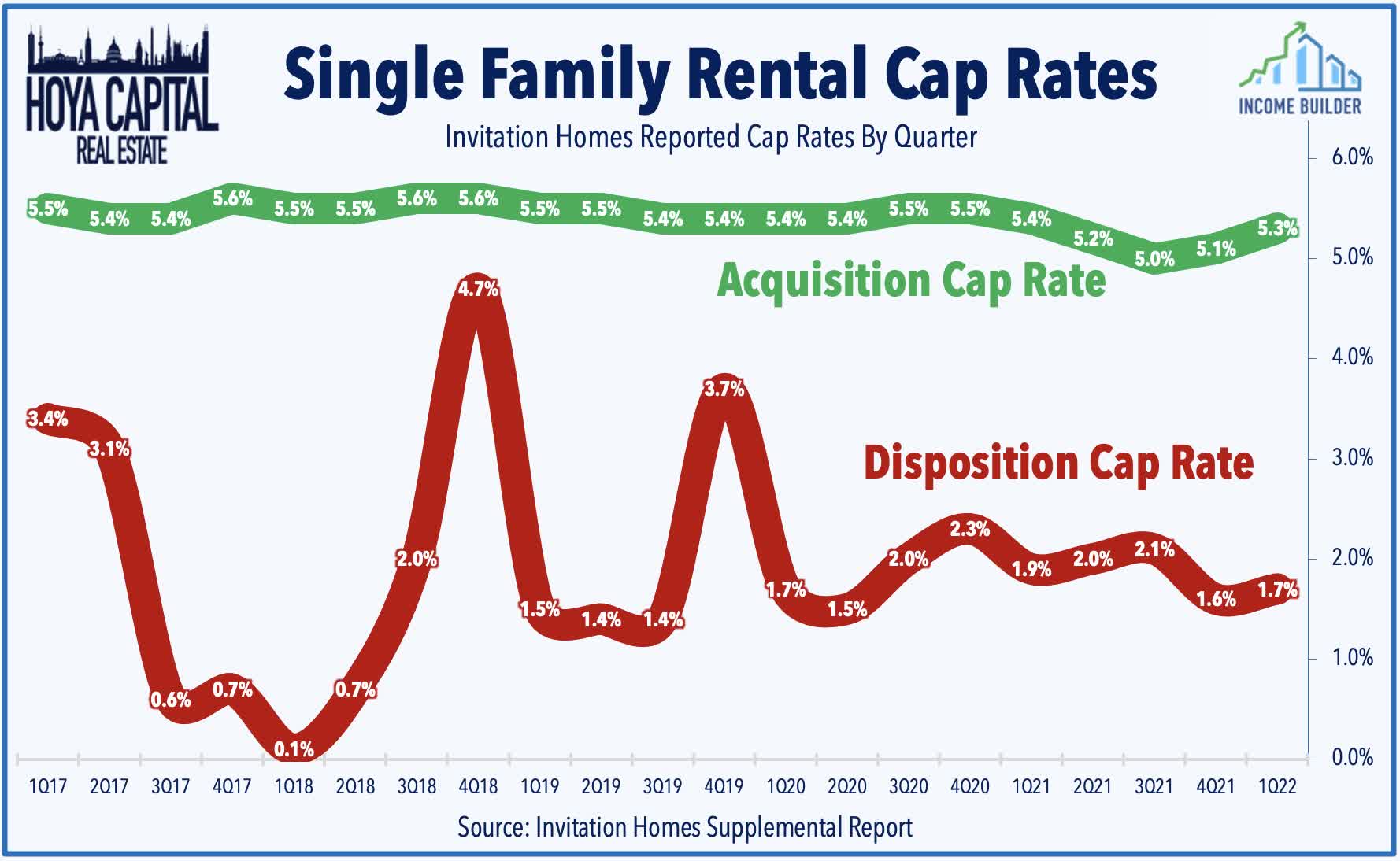

Despite the recent successes, critics continue to question the long-term sustainability of the institutional stabilized ownership model pioneered by SFR REITs, particularly if home price appreciation consistently outpaces rent growth. This can create a problematic situation for SFR REITs: Future acquisitions can become less accretive as REITs are forced to pay higher prices for the same cash flow. Meanwhile, property taxes and other expense items are generally tied to rising home values. Aided by the PropTech efficiencies discussed above, however, INVH continues to see accretive acquisition opportunities with acquisitions with cap rates in the low-5% range while it has historically sold properties with incredibly low cap rates between 1% and 3%.

Hoya Capital

Hoya Capital

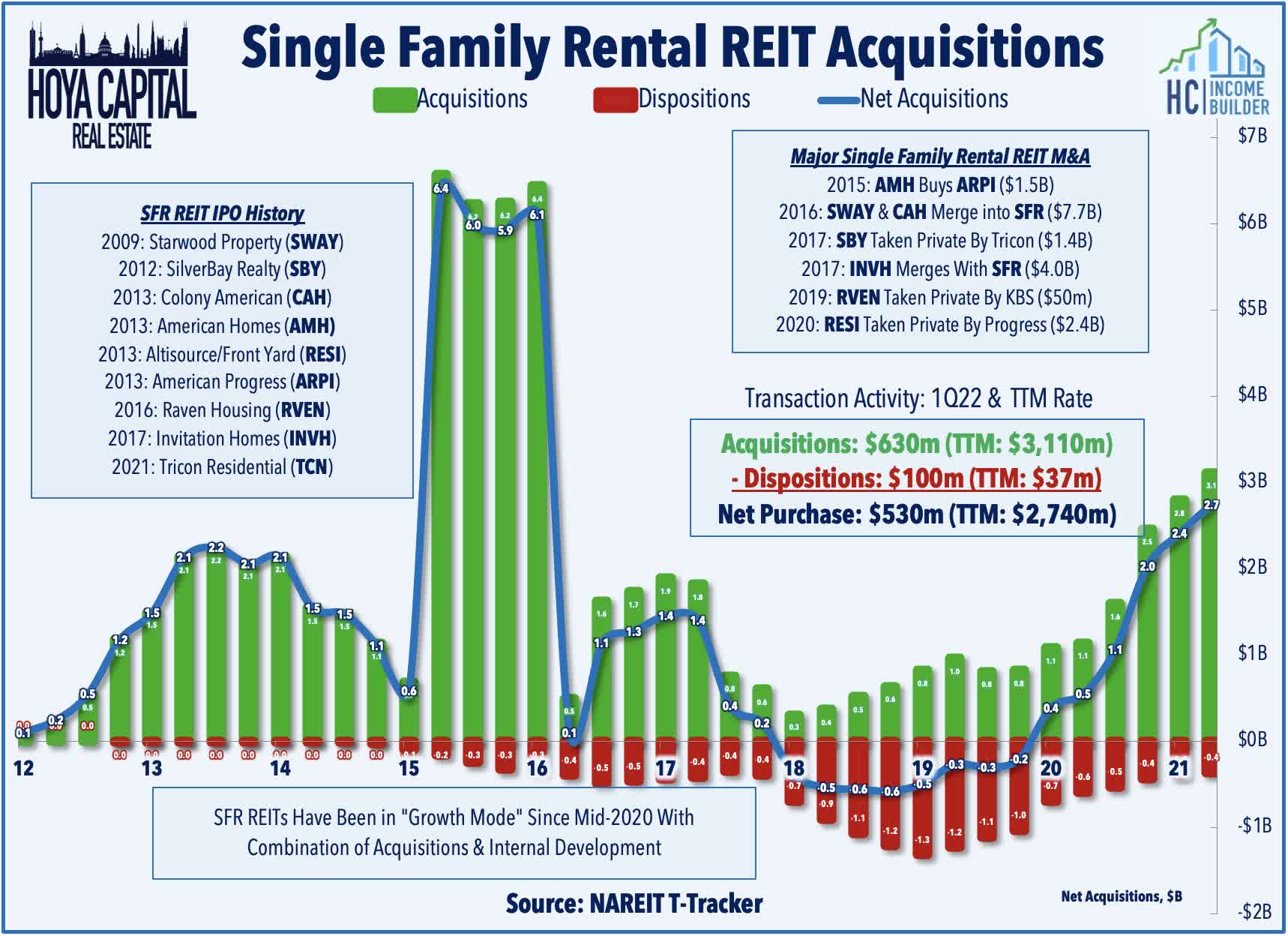

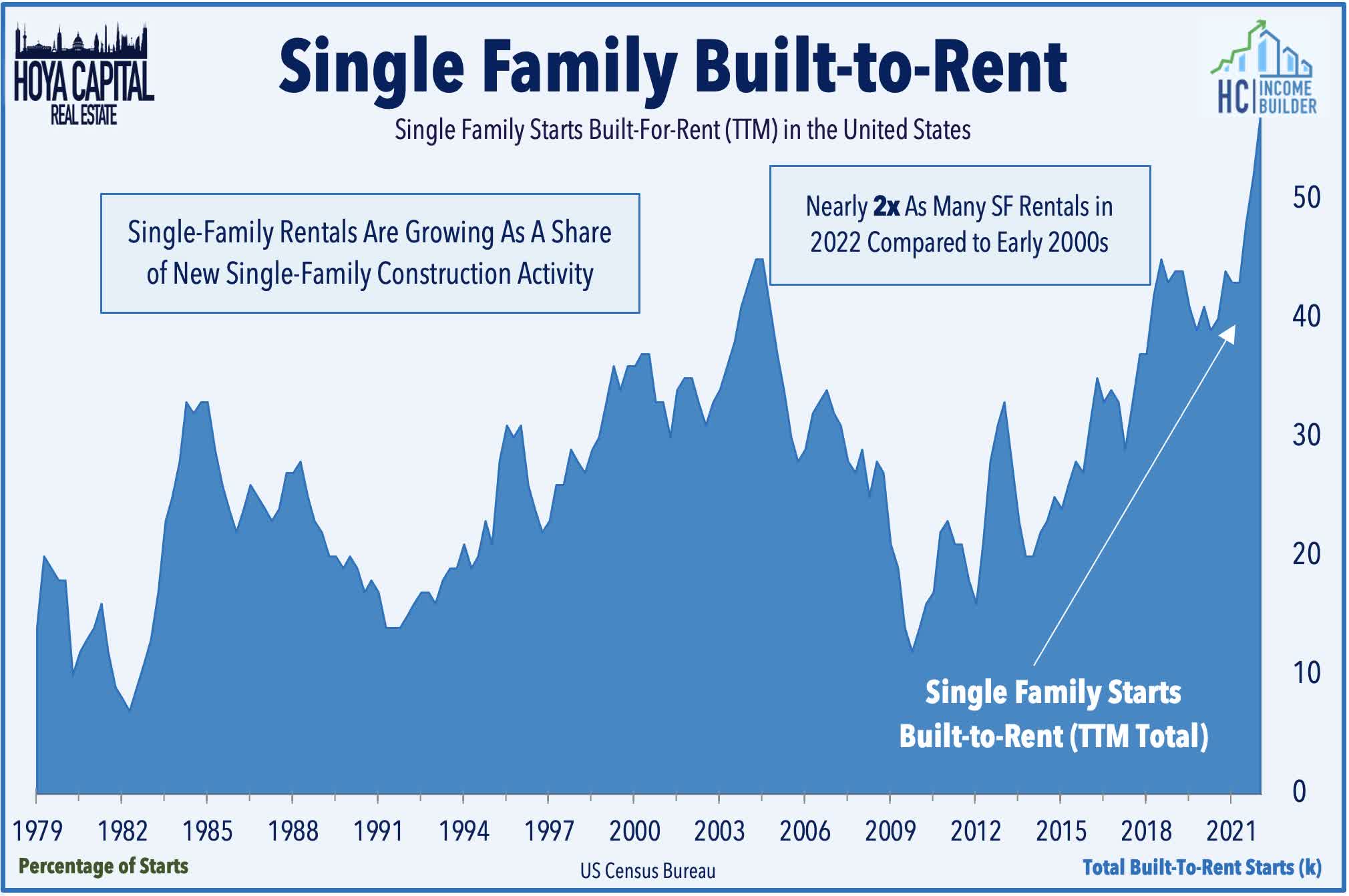

SFR REITs have switched back into “growth mode” and continue to plow ahead with external growth plans through both traditional channels and emerging growth channels ranging from ground-up internal development, partnerships with homebuilders, and the aforementioned iBuyers. Combined, these REITs have added nearly $3B in net acquisitions over the past year, the highest twelve-month total since late 2016. These three REITs combined to add more than 10,000 homes to their portfolios in 2021 led by Tricon, which added roughly 6,500 homes while American Homes added 4,600 to its portfolio in 2021 while Invitation Homes added 4,000 homes.

Hoya Capital

Hoya Capital

Rapid home price appreciation and stiff competition in the “traditional” acquisition channel have forced SFR REITs to get creative with external growth plans. “If you can’t buy it, build it” has been the recent mantra as SFR REITs have effectively become strategic homebuilders through internal development and partnerships with existing builders. AMH – which has quickly become one of the largest homebuilders in the country – built 2,054 homes in 2021 through its internal AMH Development Program and expects to deliver between 2,100 to 2,400 homes in 2022. This internal development now accounts for half of AMH’s acquisitions with the remaining 50% split between its National Builders Program (buying new homes from homebuilders) and traditional acquisitions.

Hoya Capital

Hoya Capital

INVH announced a partnership with PulteGroup (PHM) in July to buy 7,500 new built-to-rent homes. Elsewhere, Lennar (LEN) partnered with Allianz to build $4B worth of SFR homes while Toll Brothers (TOL) partnered with Equity Residential (EQR) to build $2B rental units. These REITs have also tapped into the emerging “iBuying” industry to source acquisitions through relationships and direct investments into companies like Opendoor Technologies (OPEN) and Offerpad (OPAD) and leverage data from CoreLogic, CoStar Group (CSGP), Black Knight (BKI), and Redfin (RDFN) to source accretive acquisition opportunities.

Hoya Capital

Hoya Capital

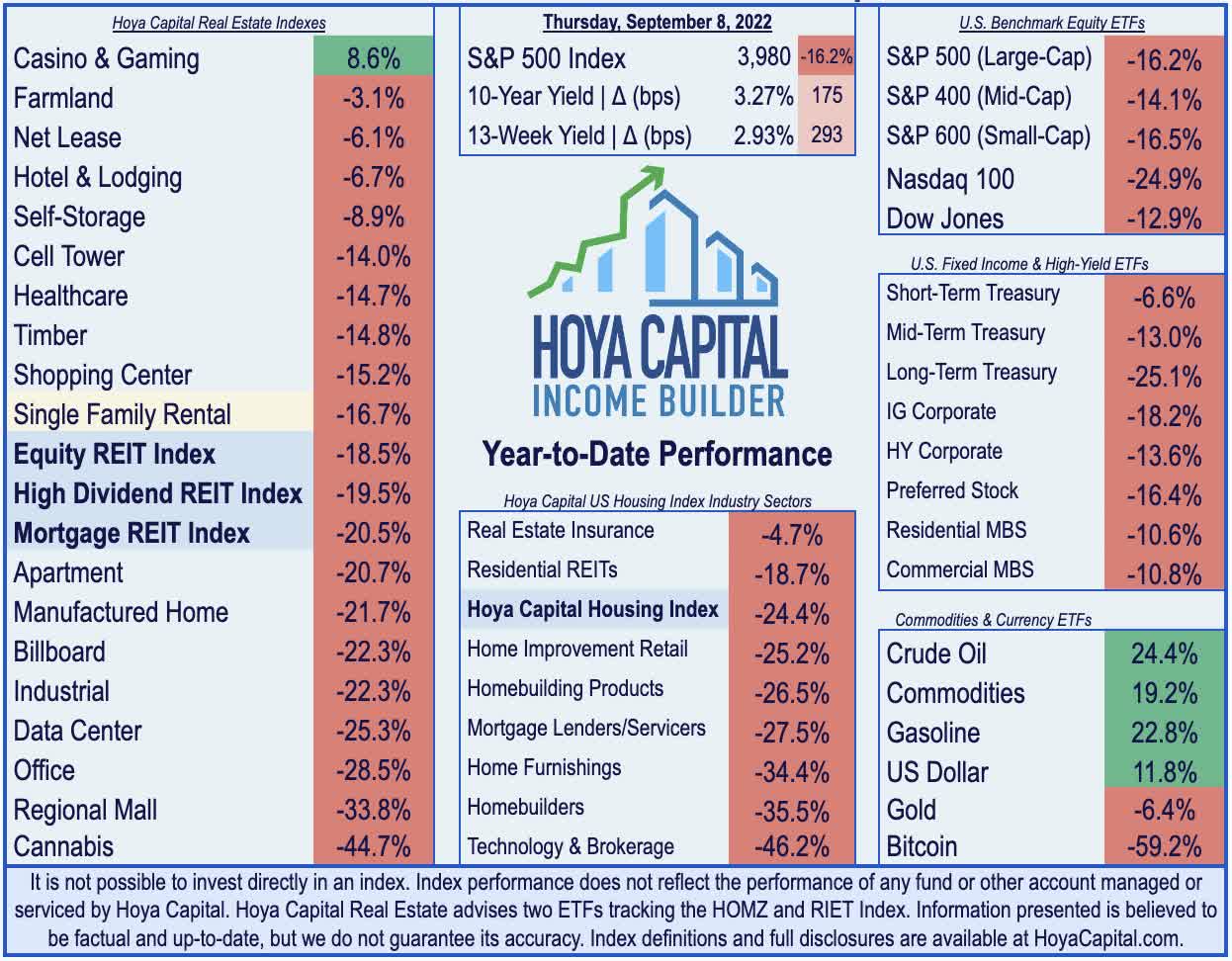

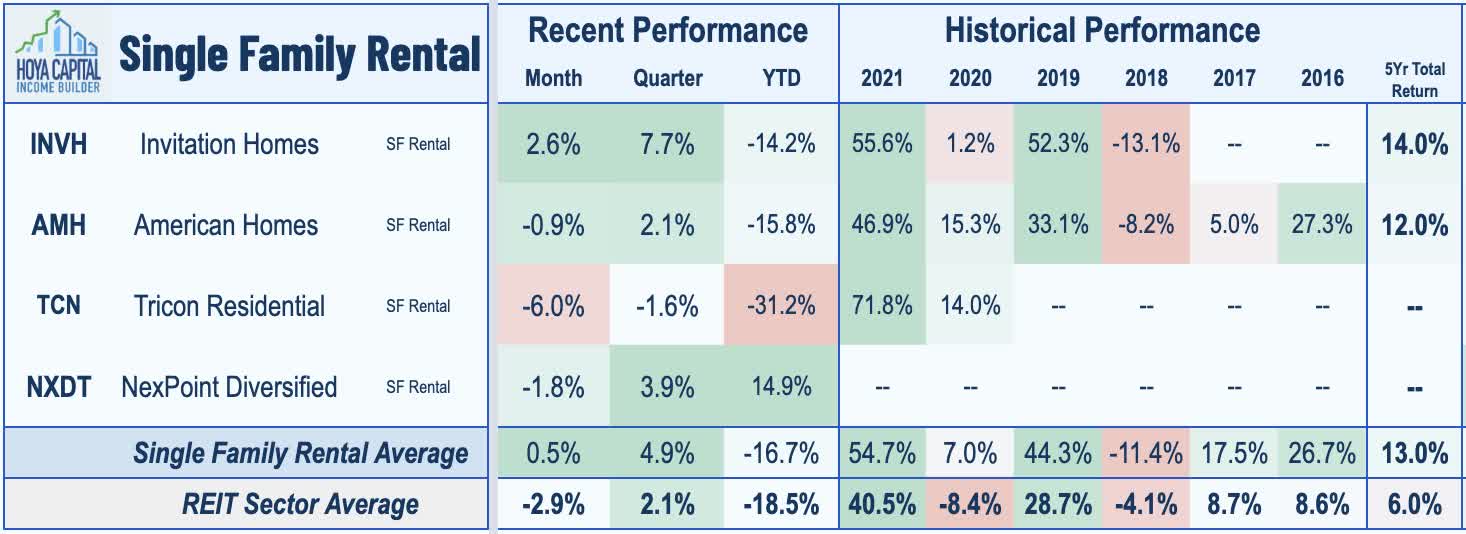

After delivering total returns of 52% in 2021, the SFR REIT sector has slumped in 2022 along with the rest of the REIT sector and broader equity market amid a historically rapid rise in interest rates. Unlike many other interest-rate-sensitive REIT sectors, however, rising interest rates and mortgage rates have historically benefited these SFR REITs as households on the margins of buying or renting tend to be pushed towards rental markets. The Hoya Capital Single-Family Rental REIT Index is lower by 16.7% in 2022, slightly outperforming the 18.5% decline from the broad-based Vanguard Real Estate ETF (VNQ) and roughly even with the 16.2% decline from the S&P 500 ETF (SPY).

Hoya Capital

Hoya Capital

Invitation Homes has been the best-performing SFR REIT this year, but remains lower by more than 14%. The Sunbelt-heavy focus of AMH and Tricon delivered superior performance in 2020 during the worst of the pandemic, but INVH delivered the most impressive performance in 2021 due, in part, to a strong rent growth rebound in its West Coast markets. On a trailing five-year basis, Invitation Homes has delivered the strongest total returns with 14.0% average annual total returns compared to 12.0% from American Homes.

Hoya Capital

Hoya Capital

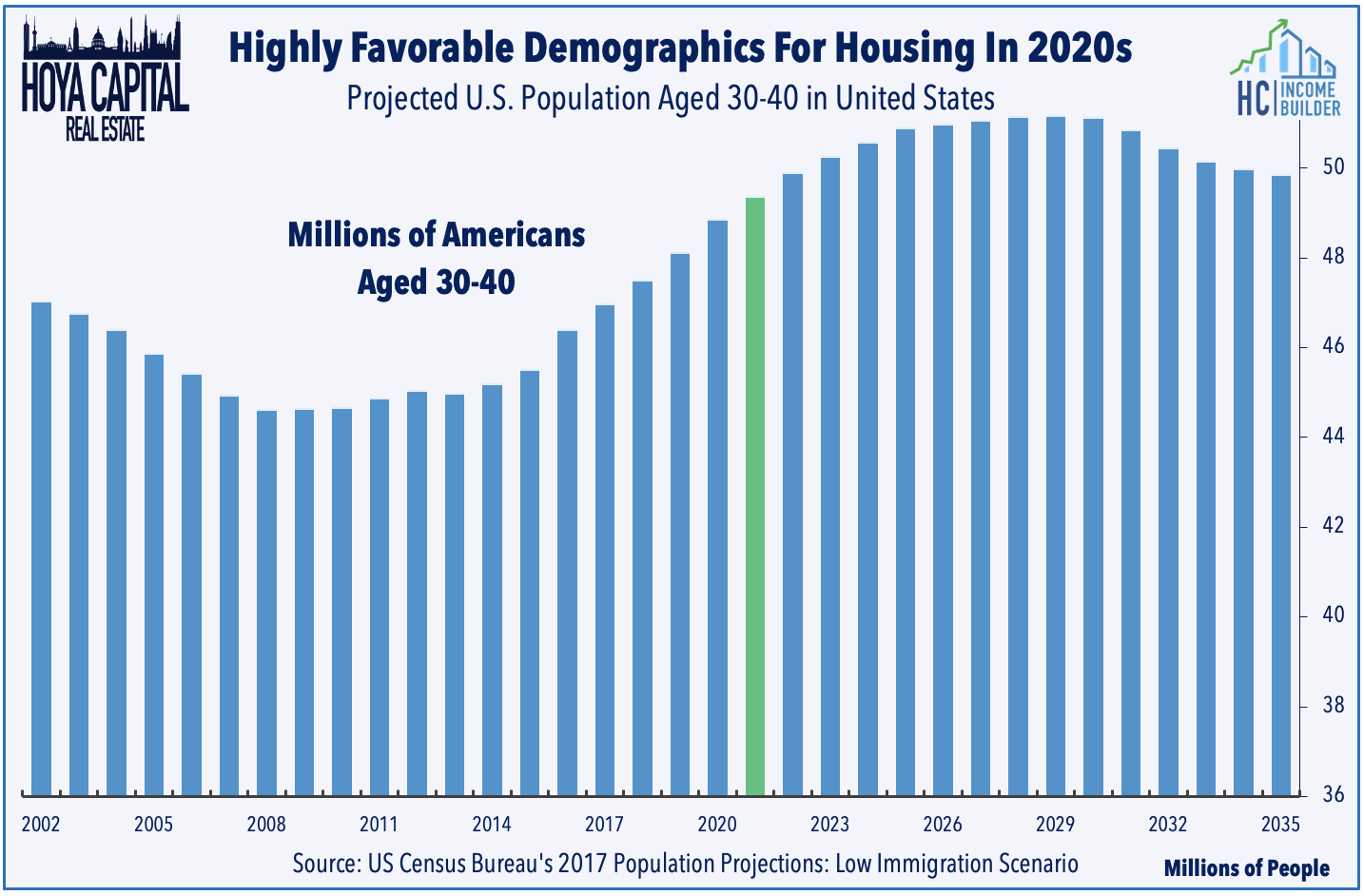

Single-family rentals, which combine the benefits of single-family living with the best parts of the multifamily experience, have become the default “starter home” for millions of Americans. Fueled by the maturing millennial generation – the largest age cohort in American history – the 2020s were already poised to be a decade of “suburban revival” and behavioral changes in the post-coronavirus world have provided an added spark and pulled some of this single-family housing demand forward. Whether they’re renting or owning, the maturing millennial generation will enter the single-family housing markets in full force throughout the 2020s in a quantity and magnitude not seen since the young boomers began to flock to the suburbs in the late 1970s.

Hoya Capital

Hoya Capital

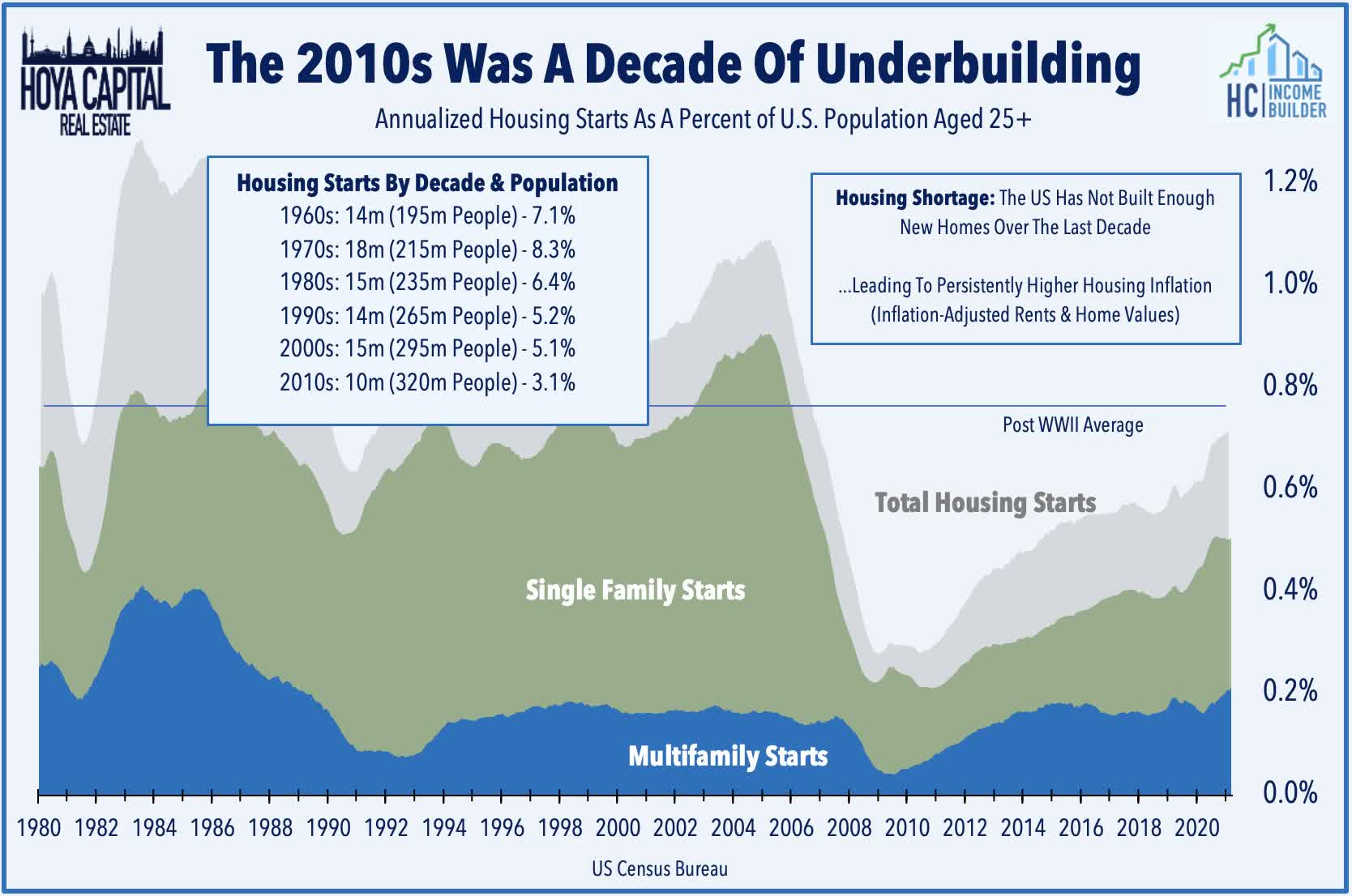

This demographic-driven demand, however, comes at a time of historically low housing supply. New home construction – particularly in the single-family category – has been historically depressed over the last decade, a result of the substantial and far-reaching fallout from the financial crisis on the residential construction industry. In the 2010s, the United States built homes at a rate that was 50% below the post-1960 average after adjusting for population growth.

Hoya Capital

Hoya Capital

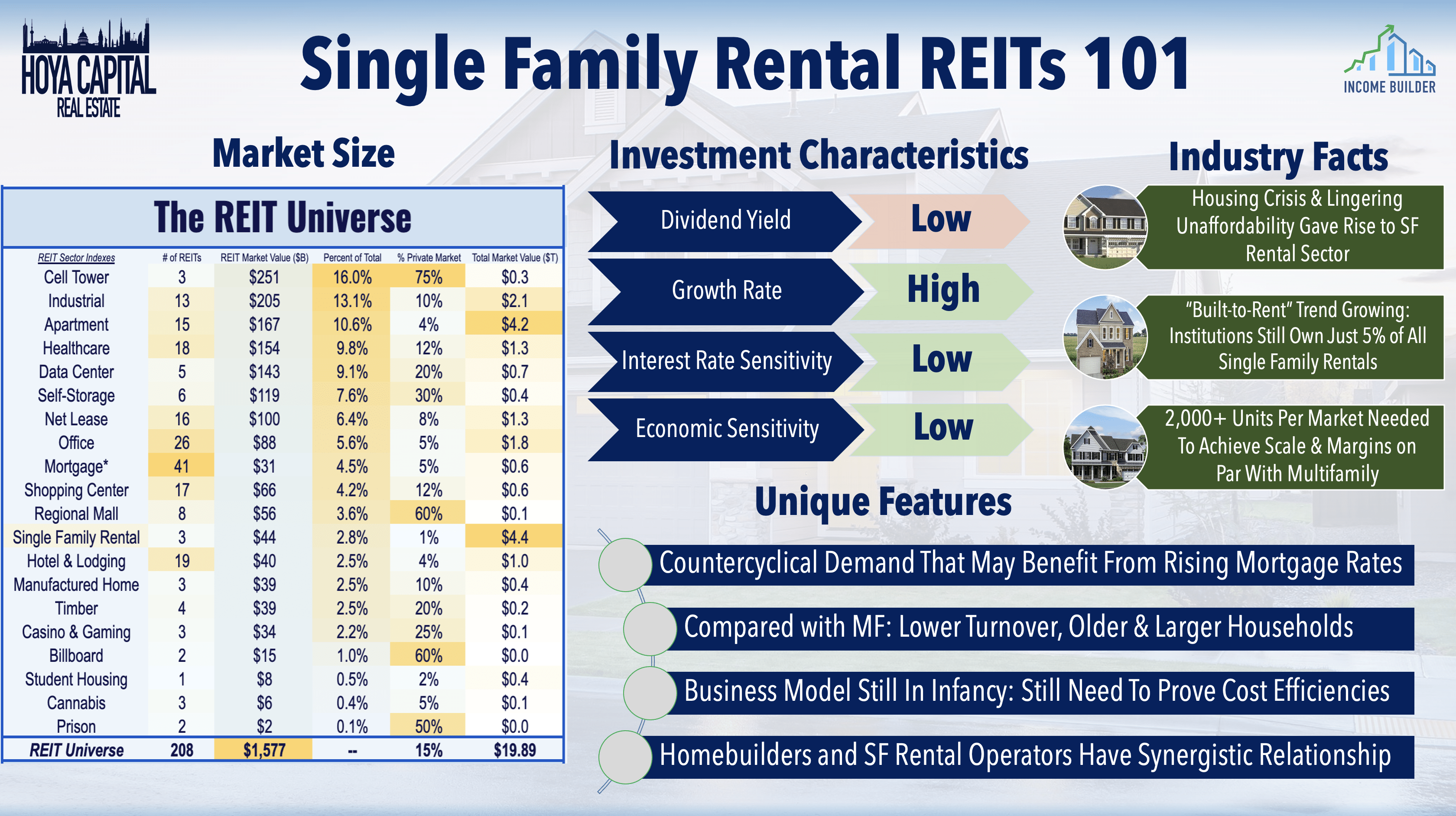

Scale is a key competitive advantage for these large institutional SFR owners, and relative to apartment buildings where each property can have several hundred units, geographical fragmentation makes it more difficult to acquire a substantial number of units to achieve scale. Density within markets is especially critical for SFR REITs for achieving efficiencies in leasing, acquisition, and maintenance. We estimate that 500-1,000 units per market are needed to achieve minimum scale, but that 2,000 units or more are needed to reach a “critical mass” whereby the REIT can localize operations within that market and achieve cost efficiencies on par with apartment REITs.

Hoya Capital

Hoya Capital

Single-family rental REITs comprise roughly 1-2% of the “Core” REIT ETFs and 5% of the Hoya Capital US Housing Index, the benchmark that tracks the performance of the US Housing Industry. Single-family rental REITs – along with their residential REIT sector peers (Apartments and Manufactured Housing REITs) – have been some of the most significant beneficiaries of the mounting shortage of housing units in the United States, and as a result, have produced same-store NOI growth that has been consistently above the REIT sector average for the past decade.

Hoya Capital

Hoya Capital

Initially, in a phase we call SFR 1.0, the SFR REIT business model depended on the bulk acquisition of distressed properties, and REITs used foreclosures as a primary source of new home acquisition. In SFR 2.0, the business model evolved into a stabilized ownership model, focused on achieving efficiencies and growing via one-off acquisitions. In SFR 3.0, we see SFR REITs mirroring the model of the larger apartment REITs with internal development teams capable of supplementing the acquisition-fueled external growth channels.

Hoya Capital

Hoya Capital

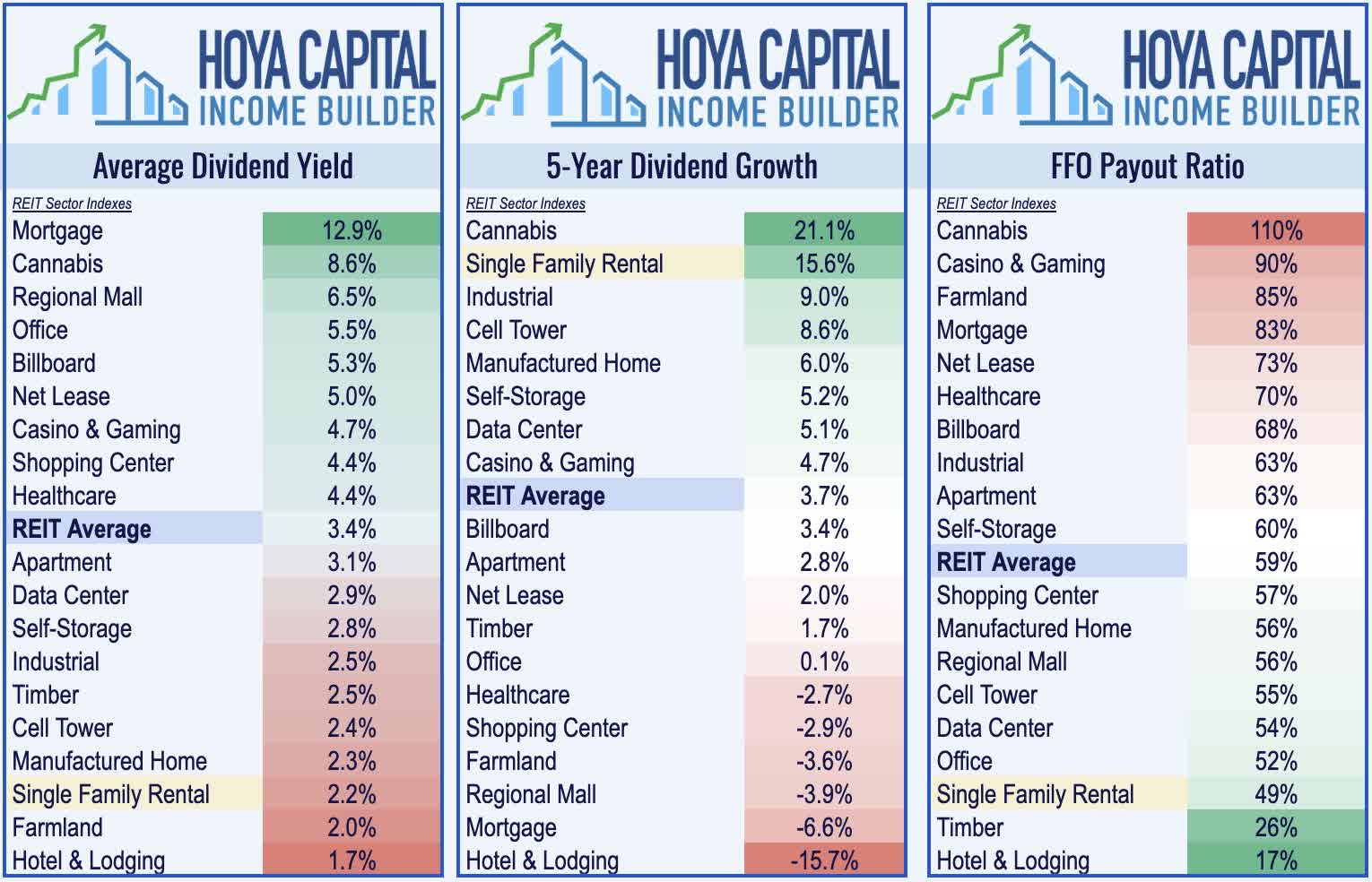

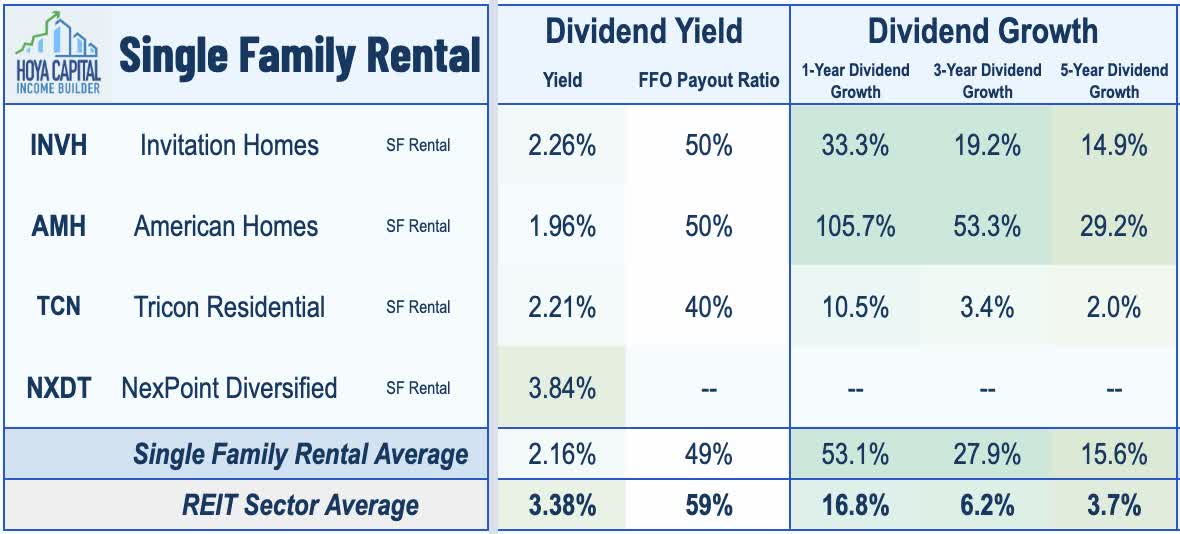

Single-Family Rental REITs are quintessential “Growth REITs” with relatively low dividend yields but with a high potential for dividend growth. Based on dividend yield, SFR REITs rank near the bottom of the REIT universe, paying an average yield of 2.2% compared to the REIT sector average of 3.4%. SFR REITs pay out just half of their available cash flow, however, and dividend growth has averaged more than 15% per year over the last five years, powered by the combination of robust external growth and strong rent growth.

Hoya Capital

Hoya Capital

Dividend growth has been especially strong over the past three years during the “pandemic era” as all three REITs have significantly raised their dividends over the past several quarters. After raising its dividend by another 30% earlier this year, Invitation Homes now pays the highest dividend yield in the SFR sector at 2.26%, followed by Tricon at 2.21% which has delivered more muted dividend growth over the past several years. American Homes pays a dividend yield of 1.96% after hiking its payout by 80% earlier this year.

Hoya Capital

Hoya Capital

Single-Family Rental REITs were born from the last economic crisis when a cascade of foreclosures enabled a new class of institutional rental operators to emerge by buying distressed properties en-masse. While home price appreciation is poised to slow considerably – and perhaps turn negative in some markets – wide distress in the U.S. housing market is highly unlikely given the underlying supply constraints resulting from a decade of underbuilding, and ironically, due in part to the broader presence of well-capitalized institutional investors. We remain bullish on the broader Single-Family Rental REIT (“SFR”) sector given the secular growth tailwinds of limited single-family supply and demographic-driven demand, attractive valuations, appealing inflation-hedging investment characteristics, and a boost in near-term demand from the historically swift surge in mortgage rates in 2022.

Hoya Capital

Hoya Capital

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Mortgage, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital

Hoya Capital

Amid the historic market volatility – and persistent inflation – our focus at Income Builder is on real income-producing asset classes that offer the opportunity for reliable income, diversification, and inflation hedging. Get started today with a Free Two-Week Trial and you can take a look at our top ideas – including our new Landowner Portfolio – and see what we’re investing in to help build sustainable portfolio income.

Subscribers gain complete access to our investment research and our suite of trackers and income-focused portfolios targeting premium dividend yields up to 10% across real income-producing asset classes.

This article was written by

Real Estate • High Yield • Dividend Growth.

Visit www.HoyaCapital.com for more information and important disclosures. Hoya Capital Research is an affiliate of Hoya Capital Real Estate (“Hoya Capital”), a research-focused Registered Investment Advisor headquartered in Rowayton, Connecticut.

Founded with a mission to make real estate more accessible to all investors, Hoya Capital specializes in managing institutional and individual portfolios of publicly traded real estate securities, focused on delivering sustainable income, diversification, and attractive total returns.

Hoya Capital Real Estate (“Hoya Capital”) is a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations is an affiliate that provides non-advisory services including research and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital has no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.

Disclosure: I/we have a beneficial long position in the shares of RIET, HOMZ, INVH, AMH, TCN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.